As the St. Patrick's Day celebrations came to an end, our attention turned to Ireland's food delivery scene. Delving into Dashmote's insights on Food Service Aggregators (FSAs) in Ireland, we wanted to explore how traditional Irish culture blends with contemporary delivery trends, shedding light on the opportunities and trends in the culinary landscape.

We gathered insights from 3 major players in the industry: JustEat Takeaway.com, Deliveroo and Uber Eats.

Ireland's food delivery landscape experienced a significant surge, with over 8,000 digital storefronts (DSFs) spread across the country witnessing an impressive 18% growth from Q1 to Q4 2023.

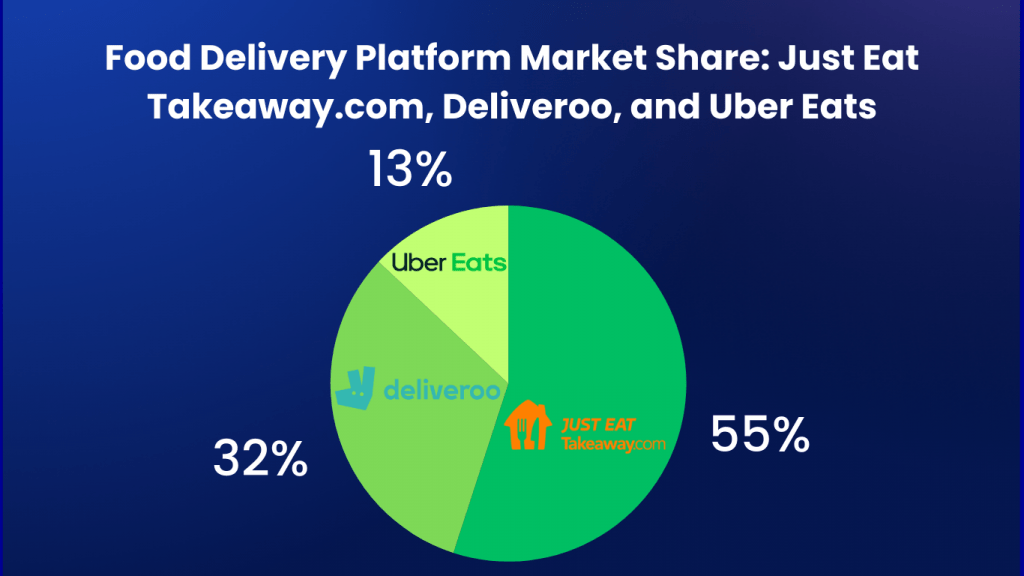

Just Eat Takeaway.com places first in the top, with a 55% market share in terms of digital storefronts within the Irish food delivery landscape, followed by Deliveroo at 32% and Uber Eats at 13%. These platforms, alike to mythical leprechauns, dominated the scene, offering a pot of gold for both consumers and businesses seeking convenient culinary experiences.

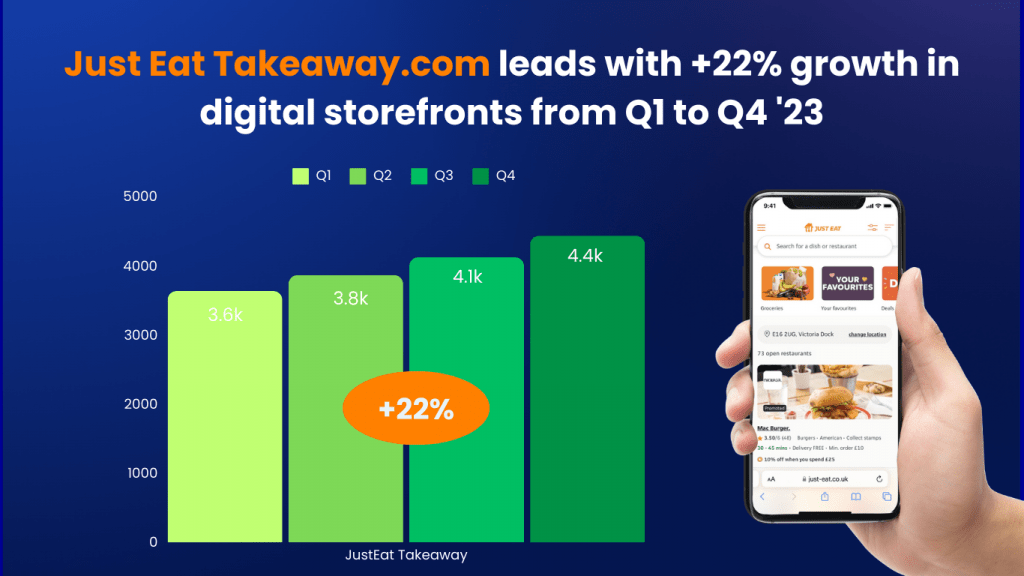

Just Eat Takeaway.com stood out as the largest and fastest growing platform, with over 4,000 digital storefronts (DSFs) and experiencing a significant growth rate in comparison to its competition, 22% growth from Q1 to Q4. With its rapid expansion, Just Eat Takeaway.com solidified its position as the go-to choice for food delivery, providing a seamless experience for both customers and restaurant partners [1].

For those who continued the celebrations at home, food delivery platforms offered plenty of options. Our analysis of the distribution of cuisine types revealed the percentage of DSFs representing each cuisine out of the total number of DSFs, and the top five preferred Irish cuisines. These include pizza (28%), burgers (24%), American fare (16%), chicken dishes (14%), and kebabs (10%). Similar to pub grub classics, these alternatives provide consumers with a flavorful feast fit for any St. Patrick's Day gathering.

As Ireland’s capital and biggest city, Dublin is the center of the country's food delivery scene, hosting 45% of its DSFs of the entire country. Dublin’s bustling streets in front of Temple Bar on St. Patrick's Day were filled with, you guessed it, beer! Guinness is the most popular choice for revelers on St. Patrick's Day, flowing freely in the heart of the city's vibrant pubs and eateries.

No St. Patrick's Day celebration would have been complete without a pint of Guinness, Ireland's beloved stout and cultural icon. With its rich brewing heritage and iconic toucan mascot, Guinness embodied the spirit of St. Patrick's Day, symbolizing Ireland's enduring influence on global beer culture. As celebrations unfolded, Guinness introduced its 'paint the town blue' campaign, offering free pints of Guinness 0.0 - a non-alcoholic version of the iconic stout - in over 800 Irish pubs until Monday, March 18. Embracing the blue color, the campaign encouraged patrons to savor the smooth taste of Guinness 0.0 and commemorate the holiday in style. Alan McAleenan, Guinness's marketing head in Ireland, expressed enthusiasm for championing Guinness 0.0 and moderation on St. Patrick's Day, fostering cultural appreciation. Partnering with Saoirse-Monica Jackson amplified this message, encouraging responsible consumption during the festivities. [2]

Fun Fact: When it comes to Guinness listings on FSA, the range is quite interesting. The least expensive Guiness is priced at 2.3€, while the most expensive one goes up to 6.0€, reflecting the diverse offerings available to Guinness lovers.

Dashmote assists enterprises in overcoming obstacles in the digital market space. As the foremost provider of big data and AI analytics solutions in the F&B sector, we enable informed strategic choices. Reach out to our team at contact@dashmote.com to establish a robust online footprint.

If you find this article valuable, you may also be interested to check out more of our blog articles on franchises, such as Empowering Heineken NL’s Online Presence Through Data-Driven Strategies and Diageo’s Digital Presence and Growth in the UK.

Follow us on LinkedIn @Dashmote to stay up-to-date with the latest food delivery data insights globally.

In the vast expanse of the American beer market, a compelling trend is emerging for FSA providers, in the form of Dry January. This abstinence-centric month has traditionally posed challenges for beer sales, but this year unveils a silver lining. Dashmote's extensive dataset provides invaluable insights into the rise of FSAs in the United States, painting a picture of shifting consumer preferences and expanding opportunities.

Every year during Dry January, beer brands face a unique challenge, but a promising opportunity. In this exploration of the US beer market, we uncover a silver lining amidst the rise of Dry January, connecting the rise of non-alcoholic beer with the dynamic growth of US food delivery. Dashmote's robust dataset guides us through the changing tides of consumer preference, presenting beer brands with a compelling narrative and strategies for success.

Dry January's Impact on Beer Consumption

The phrase "Dry January" may send shivers down the spines of beer marketers, but this year brings a glimmer of hope. According to Statista [1], the volume share of low-alcohol and non-alcoholic beer in the US next year will be about 3.2% compared to 13% in Spain, the top consuming country. Jonnie Cahill, chief marketing officer at Heineken USA, said “That tells you there's an opportunity there, because if you take a long-term view, which we've done with his innovation, which is we're in it for five, 10, 20, 50, 100 years, it's gonna get there”. By utilizing Dashmote’s intuitive app and accessing data insights, alcohol-free beer brands will be able to breach the non-alcoholic beverage market.

The Rise of Low- and No-Alcohol Beer During Dry January

The Morning Consult study, commissioned by the Beer Institute, reveals a fascinating trend among Dry January participants. In the US, about 65 percent of people between the ages of 21 and 54 said they were “somewhat to very likely” to observe Dry January. Over half of Americans opting for a dry month are turning to low- and no-alcohol beer to help them achieve their goals. Brian Crawford, the president and CEO of the Beer Institute, notes that "as many Americans increase their focus on moderate consumption, a growing majority of them are using low- and no-alcohol beer to help them hit their goals. [2]

US Food Delivery Platforms Paving the Way for Alcohol-Free Brand Success

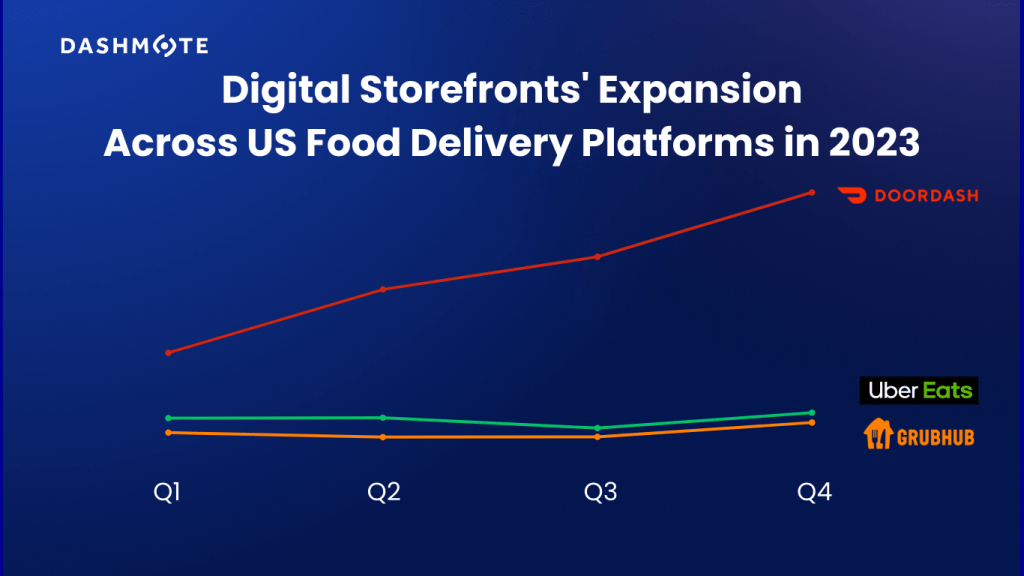

In the dynamic realm of US food delivery, the growth rates from Q3 to Q4 of 2023 present a captivating narrative for major platforms. We leveraged Dashmote’s data to check the number of DSFs present on each platform and compare them with growth rates quarter-over-quarter.

- Doordash Dominance: Doordash, a standout performer, exhibits impressive growth rates throughout 2023. In the first quarter, the FSA’s market share in the US were quite similar, standing at 400k to 460k DSFs each. The platform witnessed a substantial 9% increase from Q3 to Q4, capping off the year with an outstanding 26% surge.

- GrubHub's Resilience: Despite facing challenges earlier in the year, GrubHub demonstrates resilience in the latter part of 2023. The platform shows a commendable 2.7% growth from Q3 to Q4, showcasing its ability to adapt and maintain a steady market presence. This positive trajectory positions GrubHub as a reliable player in the evolving food delivery landscape.

- UberEats' Strategic Growth: UberEats strategically maneuvers the market dynamics, achieving a 2.8% growth from Q3 to Q4. This signifies the platform's responsiveness to evolving consumer demands and its consistent efforts to enhance its digital storefronts. UberEats concludes the year on a positive note, contributing to the overall growth in the US food delivery universe.

- Total FSA Universe Soars: Overall, between Q3 and Q4, there was a noticeable increase compared to the previous quarters for FSA (food service aggregators). Dashmote’s data unveils an impressive 10.3% growth in Q4.

Market Penetration Opportunity for Alcohol-Free Brands

The US food delivery expansion not only signifies the industry's adaptability but also presents a substantial opportunity for alcohol-free beer brands to establish a more robust presence in the market. As American consumers increasingly embrace low- and no-alcohol beer options, the US beer industry strategically positions itself to meet this growing demand. Dashmote's dataset serves as a reinforcing compass, illustrating the industry's commitment to accommodating changing consumer preferences and embracing sobriety, all while upholding the craft and quality that defines its character.

Conclusion: Riding the Wave of Non-Alcoholic Beer's Momentum

The data-driven insights unveil a promising landscape for non-alcoholic beer within the food delivery sector. Despite historical challenges during Dry January, expanding digital storefronts and overall growth in the food delivery universe highlight a positive trajectory for alcohol-free options. Breweries across the US, investing in non-alcoholic technology and processes, provide consumers with diverse choices. Dashmote's data navigates brewers through the tides of change, as the appeal of non-alcoholic beers becomes a prevailing force in the ever-evolving American beer market.

Dashmote assists enterprises in overcoming obstacles in the digital market space. As the foremost provider of big data and AI analytics solutions in the F&B sector, we enable informed strategic choices. Reach out to our team at contact@dashmote.com to establish a robust online footprint.

If you find this article valuable, you may also be interested to check out more of our blog articles on franchises, such as Heineken’s Journey in Southeast Asia and Canned Beverages Landscape of 2023.

Follow us on LinkedIn @Dashmote to stay up-to-date with the latest food delivery data insights globally.

A recent article discussing Heineken's performance in the European food delivery market highlights the brand's strong presence in the Netherlands [1]. With a market penetration hovering around 22% throughout various months in 2022 and 2023, Heineken remains the favourite beer choice for many Dutch consumers. In 2022, Heineken saw a 24% increase in operating profit and a 6.9% boost in global beer sales compared to the previous year, with their premium beers showing even stronger growth [2]. This remarkable progress shows Heineken's ongoing popularity and suggests that the brand will continue to dominate the beer market in the Netherlands for the foreseeable future.

Heineken's success can be viewed in the broader context of the Netherlands' thriving beer industry. The country has consistently been the top beer exporter in the European Union, maintaining this status for 21 years [3,4]. In 2020, the Dutch exported a substantial €1.9 billion worth of beer, with the United States, France, Britain, and Canada being the primary destinations. Rooted in the Middle Ages, the tradition of beer brewing in the Netherlands continues to thrive, evidenced by the 605 licensed breweries operating in the country in 2020, which together create a vibrant and diverse beer landscape.

Our data reveals a noteworthy drop in the number of digital storefronts (DSFs) selling beer between Q4 2022 and Q1 2023. In just a few months, the total count of beer-selling DSFs shrank by approximately 13%.

The decline in beer-selling outlets and reduced sales for some brands in Q1 2023 indicate challenges in the Dutch beer industry, stemming from shifting consumer preferences, economic factors, and rising beer prices. An increasing number of Dutch consumers are opting for alcohol-free and low-alcohol craft beers, impacting traditional beer brand sales [5]. The war in Ukraine has led to surging energy and raw material prices. Heineken, for example, raised their prices by an average of 10.7% [6,7]. These increased costs, combined with high food and energy prices, interest rate hikes, and stagnant wages, have caused households to prioritise essential goods over alcohol, contributing to the decline in beer-selling outlets in the Netherlands.

Besides Heineken, it is interesting to note that other well-established Dutch beer brands also have significant market shares according to our data. In March 2022, Amstel had a market penetration rate of 3.8%, Grolsch 2.4%, Bavaria 1.9%, Hertog Jan 1.8%, and Jupiler 1.3%. The data also shows that Heineken has the largest presence of outlets that sell its beer, followed by Amstel. Additionally, Heineken has the highest percentage of total digital storefronts among all beer brands in August 2022.

From March 2022 to February 2023, Hertog Jan and Grolsch saw the most significant growth in market share among Dutch beer brands. Hertog Jan had the largest increase of 18%, while Grolsch had a more modest increase of 1%. This positive trend suggests that these two brands have been resonating with Dutch consumers. On the other hand, Amstel, Bavaria, and Jupiler saw a decrease in their market penetration rates. It's still uncertain which brand will come out on top in the long run, but the positive trend of Hertog Jan and Grolsch in the market is definitely something to keep an eye on. It will be interesting to see how these brands continue to compete in the ever-changing beer industry.

King's Day is a national holiday that celebrates the birthday of King Willem-Alexander, and it is a day of national unity and celebration. According to DutchReview [8], drinking beer is one of the biggest attractions of King's Day, and the Dutch love their booze.

On King's Day, people in the Netherlands take to the streets to celebrate with friends and family. It's a day when people can freely wander around the city with a beer in hand, enjoying the festive atmosphere. It's worth noting that outdoor drinking is not technically allowed in the Netherlands, so King's Day is a unique occasion where people can enjoy their drinks while basking in the sunshine.

As Dashmote, we are a leading big data and AI analytics company specializing in the food & beverage industry. We empower F&B enterprises by enabling leaders and analysts to track and analyze publicly available data, ultimately contributing to informed strategic decisions for your brand. Interested in learning more about deriving market insights across food delivery and F&B?

We've also conducted a similar analysis of the most listed beer brands on food delivery platforms in each US state, showcasing our global reach and expertise. You can read the article here: https://dashmote.com/articles/beer-delivery-mapping-the-winning-brews-across-the-us/

For further inquiries or to discuss how we can help your business, please contact sales@dashmote.com.

Food delivery is taking the food and beverage (F&B) industry to new heights, that includes brewers. Heineken is a Dutch beer brand founded in 1864 when 22-year-old Gerard Adriaan Heineken purchased a brewery in Amsterdam. Today, it is one of the world’s largest and most recognizable beer brands, with its products sold in over 170 countries. As the No. 1 brewer in Europe [1], it is ramping up their results and furtherly gaining popularity thanks to delivery platforms.

Food delivery can transform the beer industry in a number of ways. Primarily, it helps the brands to expand their consumer base. It provides greater convenience and availability for consumers, allowing them to enjoy their favourite brews without the need to visit a store. In addition, it increases sales by giving the opportunity to combine drinks with food items into a combo deal.

Heineken's revenue amounted to approximately 27 billion euros in 2021 [1]. As an iconic beer brand worldwide, it is leveraging the food delivery platforms to compete in the formidable US$610 billion beer market [2]. In this article, we conduct a Heineken European case study. By leveraging Dashmote’s Data Analytics SaaS platform, we analysed the presence and growth of the brand on food delivery platforms around Europe.

Heineken is available on a variety of food delivery platforms globally, such as Just Eat Takeaway, Uber Eats, and Deliveroo. The selection of Heineken beers offered varies depending on the restaurants and stores but generally includes Heineken Lager, Heineken 0.0 Non-Alcoholic, and Heineken Silver.

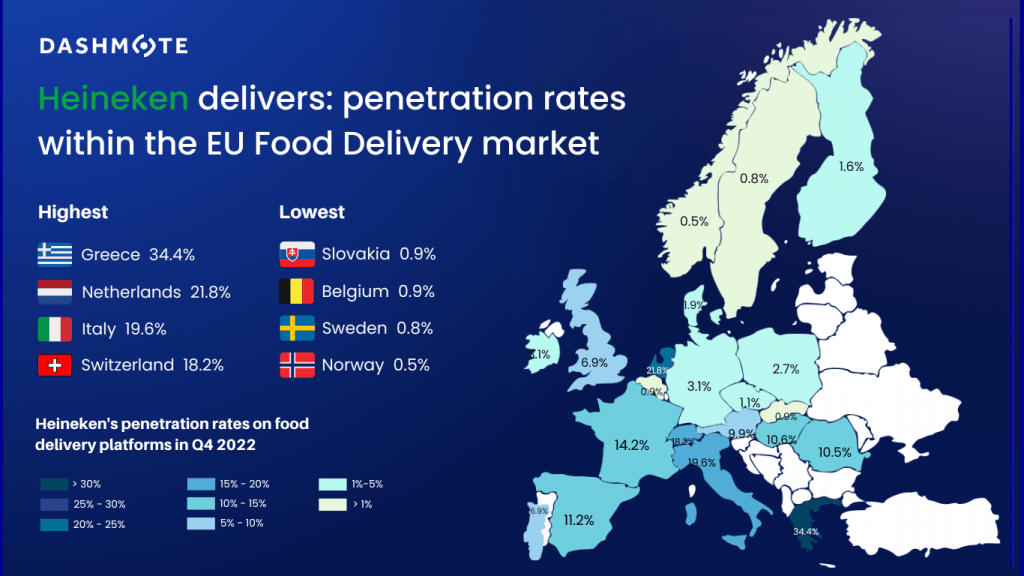

According to Dashmote’s data, surprisingly, Heineken, as a Dutch beer, does not have the highest penetration rate on Dutch delivery platforms. Remarkably, it is the most prevalent in Greece - up to 34.4% of all the digital storefronts (DSFs) in Greece sell Heineken beer. The Netherlands takes second place, with a Heineken penetration rate of 21.8%. This indicates that 1 in 5 of all DSFs on Dutch food delivery sells Heineken beer. This is followed closely by Italy (19.6%) and Switzerland (18.2%). As shown in the graph, 9 countries in Europe have a Heineken penetration rate above 10%, with a particularly strong presence in the south of Europe.

Besides its unique flavour profile and commitment to brewing quality beers, the brand is also known for its sponsorship of sporting events, including the UEFA Champions League and the Formula 1 Grand Prix. These marketing efforts further help the brand to raise awareness and boost its popularity even more in Europe. It is reasonable to believe that Heineken will keep conquering European food delivery. Compared to Coca-Cola, which has an average penetration rate of 50%, Heineken still has plenty of room and opportunities to grow in the European food delivery industry.

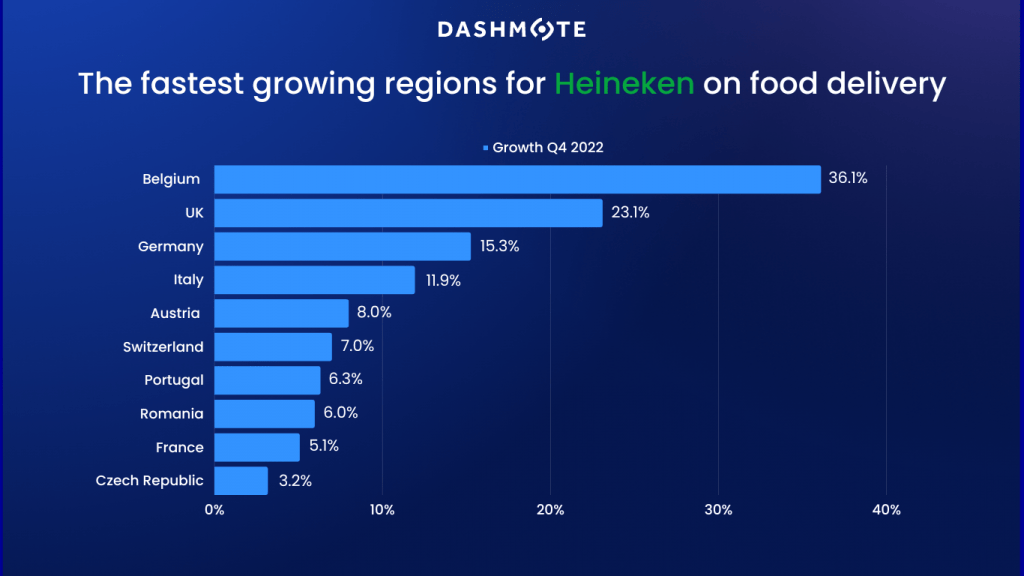

According to Dashmote’s data, most of the countries saw positive Q4 growth in DSFs listings of the brand. Belgium experienced the largest increase of 36.1%, yet its DSFs base for Heineken remained relatively small at 181 by the end of 2022. This is followed by the UK with a 23.1% growth and Germany with a 15.3% growth. Interestingly, Greece, with the highest penetration rate of 34.4%, was the only European country that saw a negative decrease in DSFs listings of 8.4% in Q4, 2022.

Dolf van den Brink, Heineken’s Chief Executive, said in a statement in October 2022 that they have seen signs of a slowdown in demand for its beer in some European markets after its third-quarter sales rose by less than expected [3]. This could be caused by the limited consumer purchasing power and beer consumption due to inflation. However, according to Dashmote’s data, we do see a fairly higher growth in some of its major markets, such as the UK and Germany. On a positive note, in the brand's 2023 forecast in August, they expected its operating profit would rise by a mid to high single-digit percentage [4].

In January 2021, Heineken 0.0 launched a global campaign, "Cheers with no alcohol. Now you can", to tap into "Dry January" and the growing market for non-alcoholic drinks at social events. The non-alcoholic beer market amounts to US$36.75 billion in 2023 and is growing annually by 12.61% (CAGR 2023-2025) [5]. Heineken is a key player in this emerging market and shows strong ambition in growing non-alcoholic beers. In fact, 7% of total volume is low or non-alcohol, which is higher than the world’s largest brewer AB InBev (6%).

According to Dashmote’s latest data, the UK has the highest Heineken 0.0 penetration rate of 3.62%. Since the penetration rate of Heineken is 6.9% in total, it indicates that more than half of the DSFs on British food delivery platforms also sell the non-alcoholic version of the beer. This is followed by the Netherlands with a Heineken 0.0 penetration rate of 2.81%, taking up to 1/10 of all the DSFs selling the brand's products. Greece (2.7%), Romania (1.3%), Spain (1.2%), and Ireland (1.1%) all had a Heineken 0.0 penetration rate above 1%.

Dashmote is the leading big data and AI analytics company in the food & beverage industry. We help F&B enterprises by empowering leaders and analysts to track and analyse publicly available data to contribute to making strategic decisions for your brand. Do you want to know more about retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.