The delivery market within the food industry has experienced an exponential amount of growth over the last couple of years. With a new Lumina Intelligence report (2022) acknowledging the use of delivery as ‘habitual to consumers’ [1]. This growth can be attributed to busy lifestyles, urbanization, digitalization, and the desire for a wide variety of culinary options. However, the food delivery space is also largely influenced by the operational challenges faced by restaurants, with approximately 60% of restaurants failing within their first year of operation, and 80% don't survive beyond five years [2]. These multifaceted factors collectively contribute to the food delivery market's status as a rapidly evolving and highly-uncertain industry.

Monitoring the newly opened and closed digital storefronts on the food delivery platforms holds significant importance for food and beverage brands. By maintaining a keen awareness within the industry, brands can identify newly established outlets, offering potential collaboration opportunities for the distribution of their products. Simultaneously, an monitoring the cessation of operations at certain digital storefronts, leading to the discontinuation of their product sales, is essential for tracking a brand's market performance.

Furthermore, it is crucial to acknowledge that restaurants do not readily alter their menu offerings, making it imperative to identify those new ventures amenable to forging fresh partnerships. Brands that fail to monitor and adapt to this changing landscape risk losing market share and relevance in the industry.

In this article, we undertake an analysis of the changes occurring in the food delivery sector in both the UK and Australia. Our examination focuses on the shifts in the digital storefront base within the dominant platforms in this industry. By leveraging Dashmote’s data, we found alarming trends of 2023 food delivery that can help your food and beverage brands to maintain their competitive edge in the market.

The UK is one of the biggest markets for food delivery, with Lumina Intelligence stating that 12% of UK adults order delivery at least once per week [3]. The projected revenue in the Online Food Delivery market in the UK is expected to experience an annual growth rate (CAGR 2023-2027) of 12.12% and reach US$40.64bn in 2023 [4]. The market is contestable although dominated by a small number of firms such as Just Eat, Uber Eats and Deliveroo. According to a global consumer survey conducted in the country in 2022, 69% of respondents used Just Eat within the past 12 months. Meanwhile, 48% of respondents used Deliveroo and Uber Eats [5].

According to Dashmote’s data, 3.9% of the digital storefronts in the UK closed during Q2. Specifically, Uber Eats saw 6.3% of its digital storefronts shutter in Q3 2023, while Deliveroo faced a 2.1% closure rate.

During the same period, it's noteworthy that the rate of newly opened digital storefronts exceeded that of closures, indicating a net growth in the food delivery market. In Q2, 5.2% of digital storefronts were opened alongside the 96.1% of existing ones, underscoring the expansion of the market. If you require precise information regarding the specific storefronts that have opened or closed, please do not hesitate to email us at contact@dashmote.com.

Revenue in the Australian food delivery market is expected to show an annual growth rate (CAGR 2023-2027) of 6.61%, resulting in a projected market volume of US$2.70bn by 2027[6]. With over 20 online food ordering and delivery platforms in Australia, the market remains a highly competitive space. Several well-known players such as Deliveroo and Foodora have already left the Australian market. Today, DoorDash, Menulog, and UberEats are considered as the most popular food delivery platforms in Australia [7].Dashmote’s data reveals that in Q2, 3.3% of digital storefronts on Uber Eats closed, with 95.6% still in operation. Notably, the rate of newly opened digital storefronts stands at 7.7%, which is more than twice the rate of closures. This data emphasizes the swift growth of the Australian food delivery market.

Dashmote is dedicated to assisting enterprises in overcoming obstacles and achieving success in the digital market space. As the foremost provider of big data and AI analytics solutions in the food and beverage (F&B) sector, we enable companies to make informed strategic choices by offering thorough analysis and invaluable insights into the food delivery market and F&B trends. Interested in taking your online business to the next level? Feel free to reach out to our team at contact@dashmote.com. Together, we can establish a robust online footprint for your Food & Beverage enterprise.

If you find this article valuable, you may also be interested to check out more of our blog articles on Uber Eats.

Follow us on LinkedIn @Dashmote to stay up-to-date with the latest food delivery data insights on a global scale.

Uber Eats is an online food ordering and delivery platform that was launched by Uber back in August 2014. It originally began in California as one of the experimental services UberFRESH to deliver convenience-store items. One year later, the platform was renamed Uber Eats. For the first time, the company has broken a product out into its own standalone app. Since then, the company has come a long way to become a significant representation of the modern digital culture. During the Covid pandemic, it had a 70% increase in gross booking and drove more than 50% of the total revenue of Uber in 2021[1]. Today, it operates in over 6,000 cities across 45 nations, and it is continuously expanding.

Few companies (Google, Amazon, Apple) can compete well in two markets at the same time. Uber has won the ride-hailing market in terms of market share. Is the company doing just as well in the food delivery market? During Uber’s recent Q3 earnings call, the company reported a revenue growth of $8.3 billion, which increased 72% YoY. Among that, Mobility Revenue grew 73% YoY and 8% QoQ to $3.8 billion, and Delivery revenue grew 24% YoY and 3% QoQ to $2.8 billion [2]. Unarguably, the solid earnings prove that Uber Eats, with over 81 million users world-widely, is succeeding in the food delivery industry [3].

In this article, we conduct an Uber Eats case study on a global scale. By leveraging Dashmote’s Data Analytics SaaS platform, we summarised a number of key features on this platform around the globe. It includes the growth of digital storefronts in Q3, the most popular cuisine types, and the top-listed beverage brands. After reading the article, you will gain a more sophisticated understanding of the general popularity of Uber Eats, and its current food and beverage trends.

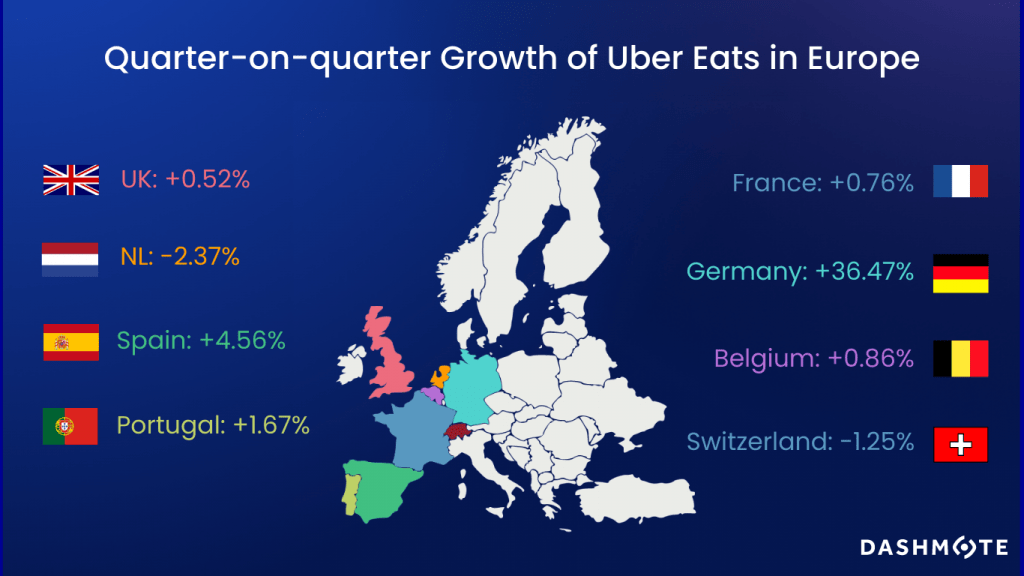

According to our Q3 food delivery data, the growth in Uber Eats‘ digital storefronts in major European countries has been slowing down. Uber Eats NL and Switzerland saw a quarter-on-quarter decrease in restaurant listings on its platform. Belgium and France grew by less than 1%. In the UK, after a double-digit growth of 10.75% in Q2, the growth in restaurant listings decreased dramatically to 0.52% in Q3. However, in Germany, it saw a staggering QoQ growth of 36.47%. This is not mistaken. In fact, the company is growing its German delivery business and plans to include 70 cities by the end of the year, expanding from its roster of 14 cities in March 2022 [4]. Our data clearly reflects this expansion.

Uber Eats is the 2nd biggest food delivery platform in the U.S., controlling over 25% of the food delivery market [5]. Our data shows that the U.S. remained the company’ largest market. It has around 450k restaurants listed on its platform and a QoQ growth of 1.85%. This restaurant base is 4 times the size in Japan.

According to Dashmote’s data, fast food, burger, and American cuisine are the dominating choices across the largest markets for Uber Eats. In NZ, Asian food ranked as the 3rd most listed cuisine type after fast food and burger.

One would expect Uber Eats France to showcase some French cuisine. Mistakenly, burgers, American, and fast food make up the top 3 cuisines in France. Moreover, Italian cuisine has been ruling the world for the last decades, but not on Uber Eats. Italian food, such as pasta and pizza, did not make it to the top 3 for most of the major countries where Uber Eats operates in.

A key takeaway from this data is that global consumers increasingly value convenient and fast food, and a key aspect driving the food delivery industry is the fast and busy life of people. Understanding the key trends on Uber Eats will benefit your business in adapting to consumer demands and discovering opportunities in the market.

Our data shows that Coca-Cola remained the biggest beverage brand on Uber Eats across all major markets. In the US and the UK, Coca-Cola is now around double the size of Pepsi in terms of brand listing. Sprite and Fanta make it to the top 5 listed brands for most of the countries that are in scope. Moreover, we discovered some dark horses in the top listed beverage brands in some major countries, as shown in the visual below.

Overall, Uber Eats, along with the online food delivery industry, has witnessed an immense expansion since the pandemic began. However, our data shows that the market growth, in terms of restaurant listings, has been slowing down in Q3 2022. This can be also reflected in Uber's Q3 revenue reports, where Delivery revenue grew 24% YoY but only 3% QoQ.

After all, Uber Eats is still a success story in the food delivery industry with growing popularity. Understanding the food and beverage trends on the platform is essential for companies that can expand into the aggregator territory. Dashmote is the leading big data and AI analytics company in the food & beverage industry. We help F&B enterprises by empowering leaders and analysts to track and analyse publicly available data to contribute to making strategic decisions for your brand. Do you want to know more about retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.