The food delivery sector is revolutionising the food and beverage (F&B) industry, even impacting renowned brewers like Heineken. Founded in 1864, Heineken, a Dutch beer company, originated when a 22-year-old named Gerard Adriaan Heineken acquired a brewery in Amsterdam. Presently, it stands as one of the globe's most prominent and easily recognizable beer brands, with its products distributed in more than 170 countries. As a leading brewing group with the second largest production volume worldwide [1], it is bolstering its performance and experiencing increased popularity from leveraging the food delivery platforms.

The beer market in Southeast Asia amounts to US$23.63bn in 2023. The market is expected to grow annually by 6.74% (CAGR 2023-2027) [2]. The area exhibits a growing inclination among consumers for alcoholic drinks, alongside a rising desire for low-alcohol and non-alcoholic beers. Heineken's strategic move into the food delivery sector with its original and non-alcoholic products aligns with these trends, showcasing their forward-looking strategy to remain relevant and easily reachable in the swiftly changing environment.

In this article, we conduct a Heineken Southeast Asian case study. By leveraging Dashmote’s Data Analytics SaaS platform, we analysed Heineken’s presence and growth on food delivery platforms throughout 7 key markets.

Heineken can be found on various food delivery platforms in Southeast Asia, including Gojek, Grab, Lineman, and many more. The specific Heineken beer options available may vary depending on the restaurants and stores, but they typically include Heineken Lager, Heineken 0.0 Non-Alcoholic, and Heineken Silver.

According to Dashmote's data, Heineken has a food delivery beer presence exceeding 30% in 3 out of 7 countries in the current analysis. Notably, Heineken holds a strong position on Vietnamese food delivery platforms, where 64.1% of digital storefronts which sell beers also feature Heineken products. The Philippines ranks second, with a 35.5% beer penetration rate, meaning that 1 in 3 beer-selling restaurants on food delivery platforms offers Heineken. Singapore follows closely with a penetration rate of 31.1%. It's worth mentioning that Heineken's presence in Indonesia (11.2%) and Thailand (8.1%) remains relatively low due to distinct drinking customs and alcohol consumption regulations in these regions.

Since the above analysis pertains to digital storefronts specifically selling beers rather than encompassing all digital storefronts on the platforms, it's essential to recognize that the beer market presence in Southeast Asia remains relatively limited on food delivery, ranging from 0.71% in Indonesia to 11.3% in Singapore. In contrast, when compared to Europe, where 9 countries have a Heineken presence exceeding 10% across all digital storefronts in the respective nation, Heineken still has room for gradual expansion to attain a more substantial foothold in the Southeast Asian market.

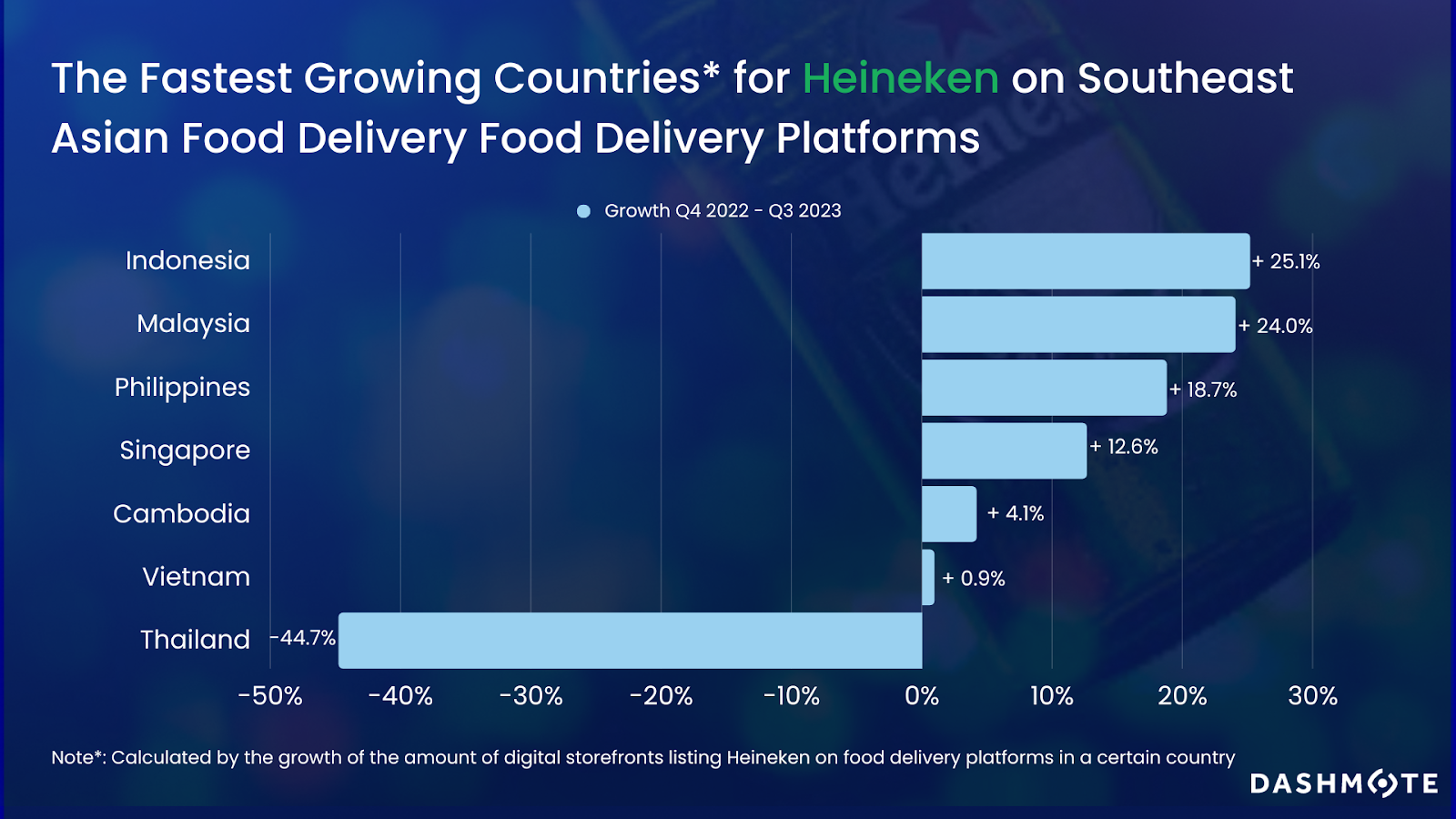

Based on Dashmote’s data, a majority of countries have witnessed a noteworthy growth in Heineken’s digital storefront listings on food delivery platforms spanning from Q4 2022 to Q3 2023. Indonesia experienced the largest increase of 25.1%. Following closely is Malaysia, exhibiting a remarkable growth of 24.0%, and Philippines with a commendable 18.7% expansion. Vietnam, although with the largest digital storefront base for Heineken, demonstrated the lowest positive growth of 0.9% over the past three quarters. Conversely, Thailand (-44.7%) encountered substantial declines in Heineken's digital storefront listings, which stands out as an intriguing exception among this trend of growth.

Upon scrutinising the data, it becomes apparent that the decline in the number of digital storefronts offering Heineken in Thailand is predominantly attributable to external factors rather than inherent issues with the brand itself. For example, the reduction of over 400 stores of Mini Big C, a convenience store in Thailand, on food delivery platforms during the timeframe under examination directly impacted the decrease in digital storefronts selling Heineken. This highlights that Heineken's performance in food delivery is significantly influenced by the broader market conditions and underlying macroeconomic variables.

In Southeast Asia, consumers who prioritise their health are actively looking for beer alternatives that offer reduced alcohol content or are entirely alcohol-free. The Non-Alcoholic Beer market in Southeast Asia is currently valued at US$1.91 billion in 2023, and it is projected to experience an annual growth rate of 8.84% (CAGR 2023-2027) [3]. In the midst of this expanding trend, Heineken 0.0 emerges as an ideal choice for those pursuing wellness and healthier living.

Dashmote's data reveals the promising early stages of Heineken 0.0's presence on Southeast Asian food delivery platforms. While it has already established itself in several countries, it has yet to make inroads into markets like Indonesia and Cambodia.

In Vietnam, Heineken 0.0 enjoys the most substantial digital presence, with 17.9% of digital storefronts selling beer offering this product. This achievement follows an impressive 60.1% digital growth from Q4 2022 to Q3 2023. Similarly, Singapore has seen a noteworthy increase of 79.7% in digital storefront listings for Heineken 0.0, resulting in a beer penetration rate of 7.2% in Q3 2023. In Malaysia, Heineken 0.0 also experienced a notable rise of 40.3% in digital storefront listings, even though its beer penetration rate remains relatively modest at 2.5%.

Dashmote is dedicated to assisting enterprises in overcoming obstacles and achieving success in the digital market. As the foremost provider of big data and AI analytics solutions in the food and beverage (F&B) sector, we enable brands to make informed strategic choices by offering thorough analysis and invaluable insights into the food delivery market and F&B trends. Interested in taking your online business to the next level? Please reach out to our team at contact@dashmote.com.

If you find this article valuable, you may wish to check out more of our blog articles on other beer brands, such as Carlsberg and Heineken in Europe.

The proliferation of the internet and the rise of shared mobility solutions have transformed Southeast Asia (SEA) in a number of ways. This includes accelerating the great expansion of the food delivery business. Just over a decade ago, 80% of Southeast Asians had no or limited access to the internet [1]. Whereas today SEA is a vibrant emerging market with over 400 million internet users and a booming digital economy [2].

Statistics indicate that the food delivery industry in SEA is experiencing an upsurge in growth due to changing consumer habits. This shift is creating promising opportunities for market players in the region. In fact, revenue in the Southeast Asian Online Food Delivery market is expected to show an annual growth rate (CAGR 2023-2027) of 17.54%, resulting in a projected market volume of US$45.53 billion by 2027 [3]. For an emerging and increasingly time-conscious middle class in SEA, having ready-to-eat meals delivered to one’s doorstep has become the norm in contemporary society.

The demand for food delivery services has exploded particularly during the pandemic. The gross merchandise value of food delivery platforms in SEA has increased by 183% in 2020 [4]. However, the industry is undergoing rapid changes as restaurant dining returns after the pandemic. SEA’s online food delivery spending rose 5% to $16.3 billion in 2022, presenting the smallest gain since 2018 [5].

In the ever-changing landscape of SEA food delivery, what were the latest trends in 2022? Who were the key players, and how were their performances? Following the European Food Delivery Race, we are expanding the series into a new scope. In this article, we leveraged Dashmote’s Data Analytics SaaS platform and reported on the statistics from 7 major markets in SEA- Indonesia, Cambodia, Malaysia, Philippines, Singapore, Thailand, and Vietnam to answer the above questions.

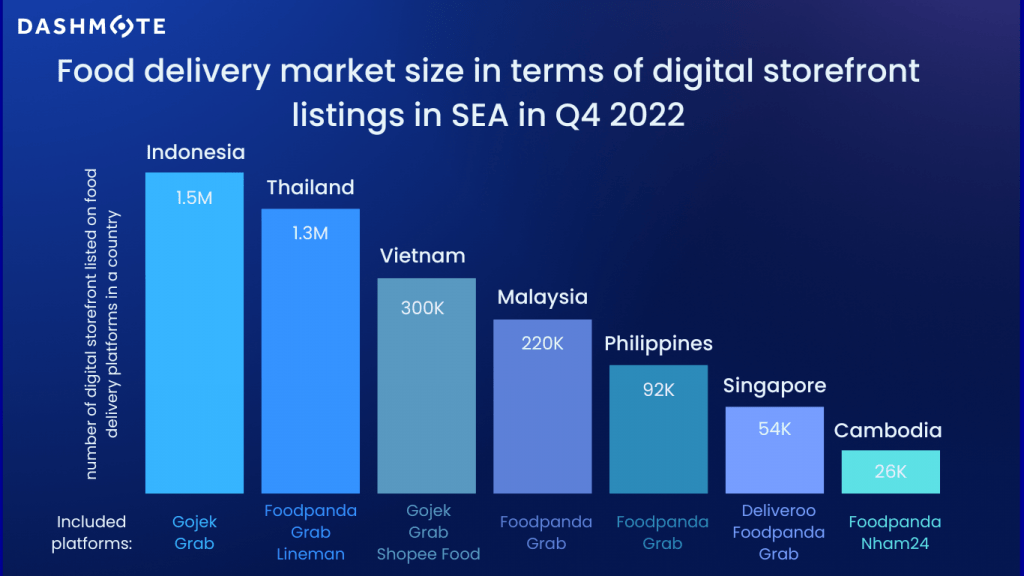

According to Dashmote’s Q3 data, Indonesia has by far the biggest food delivery market in SEA, with more than 1.5 millions Digital Storefronts (DSFs) across its major delivery platforms. Dividing this number by the total Indonesian population, we could see that there are around 535 DSFs per 100,000 population. The revenue from Indonesian food delivery is projected to reach US$1,623 million by 2026 [6]. Companies engaged in food delivery services started to thrive in Indonesia in 2015 [7]. The two big players in this sector are Gojek and Grab. Our data shows that Grab is the most significant player in Indonesia in terms of market share and growth, taking up around 74.7% of the total restaurant base in Indonesia in 2022.

The second largest market in SEA is Thailand, with 1.3 millions DSFs on food delivery. However, with a much smaller population than Indonesia, there are around 1887 DSFs per 100,000 population. Lineman is its biggest player, with 858K DSFs on its platform in Q4, 2022. This is followed by Grab, with over 323K DSFs on its platform. One may notice the good performance of Grab in many of the SEA countries. In fact, Grab merged with Uber Technologies for its Southeast Asian business in 2018 [8]. Through this acquisition, Grab also took over Uber’s network in the region and geared up to be a pan-regional food delivery platform in SEA.

The rest of the top 5 food delivery markets in SEA are Vietnam, Malaysia, and the Philippines. They all have a relatively small DSFs base (much below 1 million) compared to the 2 biggest markets. In Vietnam, the dominant food delivery platform is Shopee Food, with 182K DSFs on its platform. Whereas in Malaysia and the Philippines, Grab and Foodpanda strive to be the market leader with minor differences in DSFs listings.

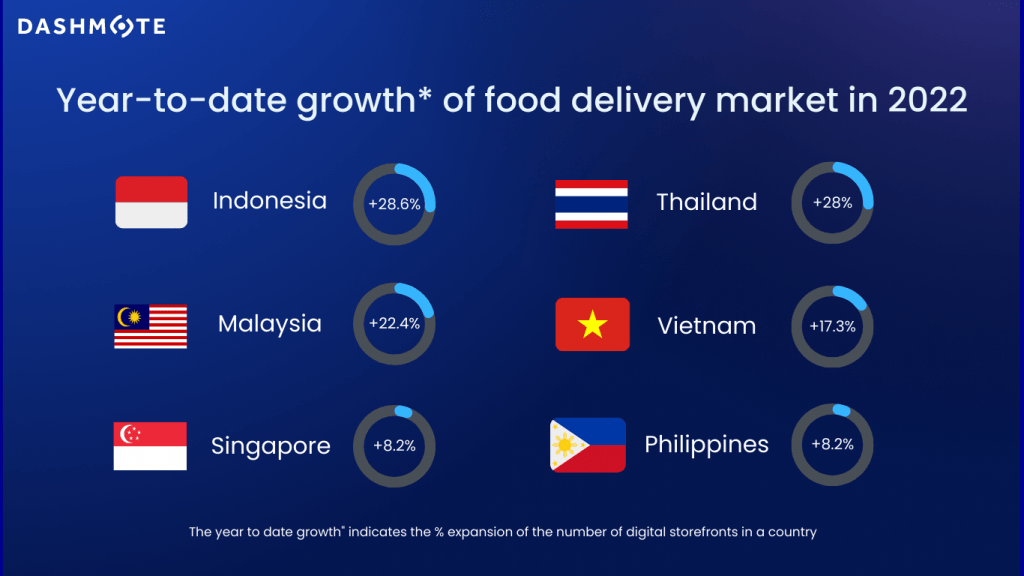

According to Dashmote’s data, all 6 markets saw positive year-to-date growth in DSFs listings. The biggest market, Indonesia, also saw the largest average growth of 28.6%. The 34.3% growth of Grab and the 14.3% growth of Gojek made up the total growth. Competition in the food delivery industry in Indonesia is getting tougher as many platforms are eyeing the food market. Maxim, Shopee Food, and Traveloka Eat have also entered the market, planning to take a piece of the pie from the huge profit potential in Indonesia.

The second biggest food delivery market in SEA, Thailand, is following closely in this food delivery race with a 28% year-to-date growth in DSFs listings. In Thailand, both Lineman and Grab grew by over 30% in 2022. However, Foodpanda decreased by 4.6% in DSFs listings. Having an European root, Foodpanda entered the SEA market in 2012 and became the pioneer in the food delivery sector in this region. However, Foodpanda had a hard time further penetrating the market as the competition became increasingly fierce. In fact, Foodpanda even shut down its Vietnamese business in 2015.

Singapore and the Philippines fall behind in the SEA food delivery race with a nuanced 8.2% year-to-date growth. In Singapore, only Deliveroo grew rapidly in 2022 by 26%. Whereas Foodpanda and Grab only saw a small growth below 5%. In the Philippines, Foodpanda also had a challenging time with a 2.6% reduction in its DSFs listings. Overall, it’s clear that the rapid growth of the SEA food delivery market was softened in 2022.

The intense race between food delivery platforms in the dynamic landscape of SEA food delivery brings huge opportunities for food and beverage brands to expand digitally and reach a wider consumer base. Unlocking these opportunities requires constant tracking and analysing of the latest data to gain a sophisticated understanding of where the market is heading. Dashmote is the leading big data and AI analytics company in the food & beverage industry. We help F&B enterprises by empowering leaders and analysts to track and analyse publicly available data to contribute to making strategic decisions for your brand. Are you interested in retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.