Hard seltzer is a ready-to-drink beverage that blends carbonated water, alcohol, and fruit flavouring in a can for portability. The absolute explosion in interest around low and non-alcoholic beverages began during the White Claws Summer of 2019. A hard seltzer brand White Claws collaborated with comedian Trevor Wallace. Together, they released a video that popularised the phrase “ain’t no laws when you’re drinking Claws”. This line led to an explosion of growth in White Claw sales that even caused shortages across the US [1].

One year later, White Claw was still dominating the sales. At the same time, more than 150 brands were bursting out in the US in the same beverage category. This including Truly, Bud Light Seltzer, Polar Seltzer, and many more. Marketed as healthy, aspirational and gender-neutral, in 2021 the global hard seltzer market size was valued at USD 8.95 billion and is expected to expand at a compound annual growth rate (CAGR) of 22.9% from 2022 to 2030 [2].

The boom of this new drink category has greatly benefited from the outbreak of the COVID-19 pandemic. Back then, consumers started to gain higher health consciousness and look for low-alcohol beverages. Moreover, millennials and the younger generation during lockdown were driven to look for novelty on the shelves at grocery stores, and the colourful, fruity-flavoured, low alcohol and calorie seltzers were the perfect eye-catcher [3]. However, in July 2022, while crowds were returning to bars and restaurants, hard seltzer sales in retail stores were down about 18%, compared to the previous year [4]. Today, some argue that this type of drinks has lost its fizz. Others expect the market to be continuously expanding into a competitive landscape.

This article provides insight into the above controversy by leveraging Dashmote’s Data Analytics SaaS platform. In this article, we evaluated the performance of the major brands on food delivery in North America. We analyzed the data from 3 perspectives: the growths, the penetration rates and the market shares in 2022.

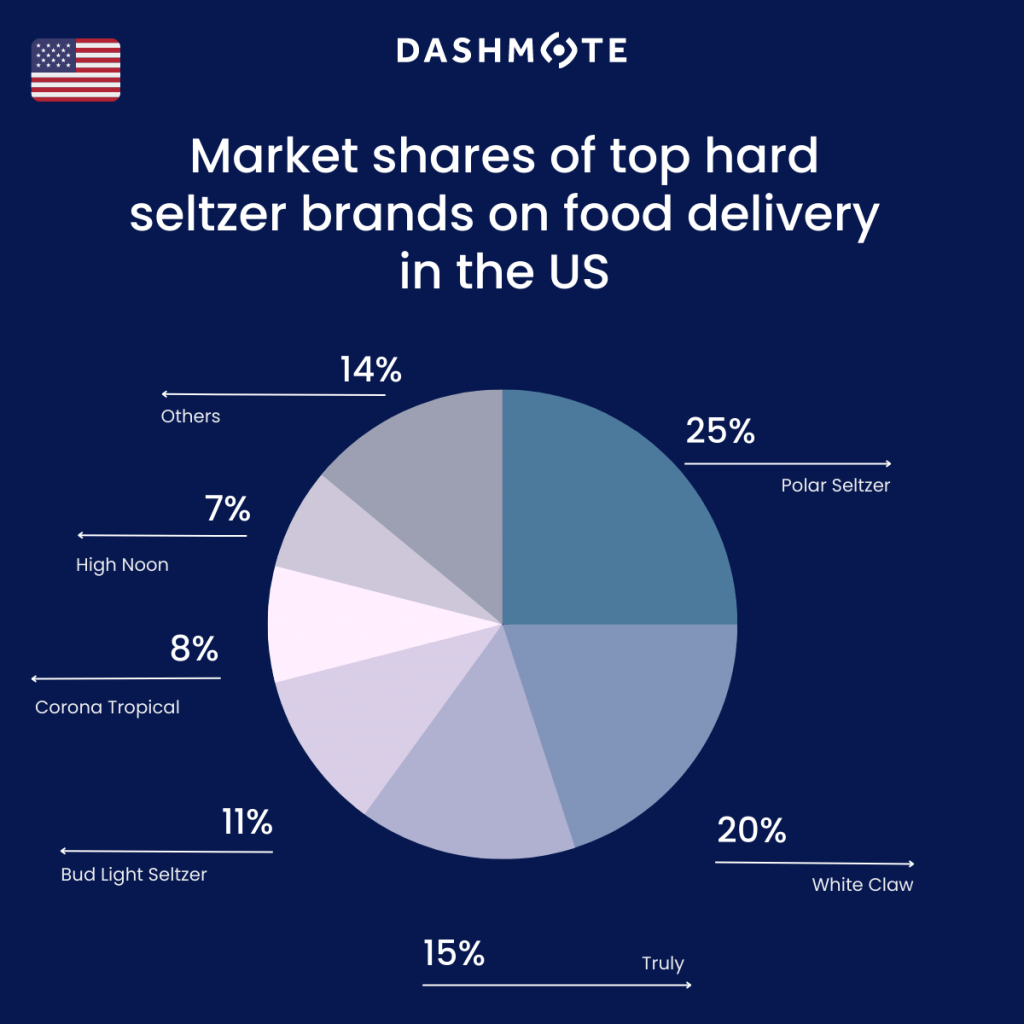

North America accounted for the largest hard seltzer revenue share of more than 55.5% in 2021 and is likely to further increase the consumption of hard seltzer in the coming years [5]. According to Dashmote’s latest data, the most listed brand on US food delivery platforms in Q4, 2022 was Polar Seltzer. It has a market share of 25% among all the Digital Storefronts (DSFs) selling hard seltzers. This was followed by White Claw, with a market share of 20%, and Truly (15%). The top 3 brands all had a penetration rate above 1% among all the DSFs in the US. Specifically, they were 2.1% (Polar Seltzer), 1.7% (White Claw), and 1.3% (Truly).

Topo Chico, bought by Coca-Cola in 2017, saw the largest quarter-over-quarter (QoQ) growth of 49% in DSFs listings in Q4, 2022. Controlling a 6% hard seltzer market share on US food delivery, Topo Chico ranked 7th among the top hard seltzer brands.

Wine and Spirit Industry Giant E&J Gallo Winery launched High Noon in 2019. It also saw a large QoQ growth of 41% and controlled 7% hard seltzer market shares in Q4, 2022. High Noon separates itself by appealing to the better-for-you crowd, including distilled liquor and real juice in its transparent ingredient list [6]. This marketing strategy appears to be successful, as proved by the growth rate in our data.

Furthermore, White Claw, Truly, and Bud Light Seltzer, all had a QoQ growth above 20%. A key takeaway from this is that the hard seltzer industry is unlikely to fizzle out in the upcoming years. Although appearing as a summertime drink, the hard seltzer market tends to remain dynamic all year round in 2022. In fact, the penetration rates of top hard seltzer brands on US food delivery are already more than 10 times higher than non-alcoholic beers, but still mainly under 2%. Partnering with restaurants and major delivery aggregators would be beneficial for hard seltzer brands to expand their digital footprints.

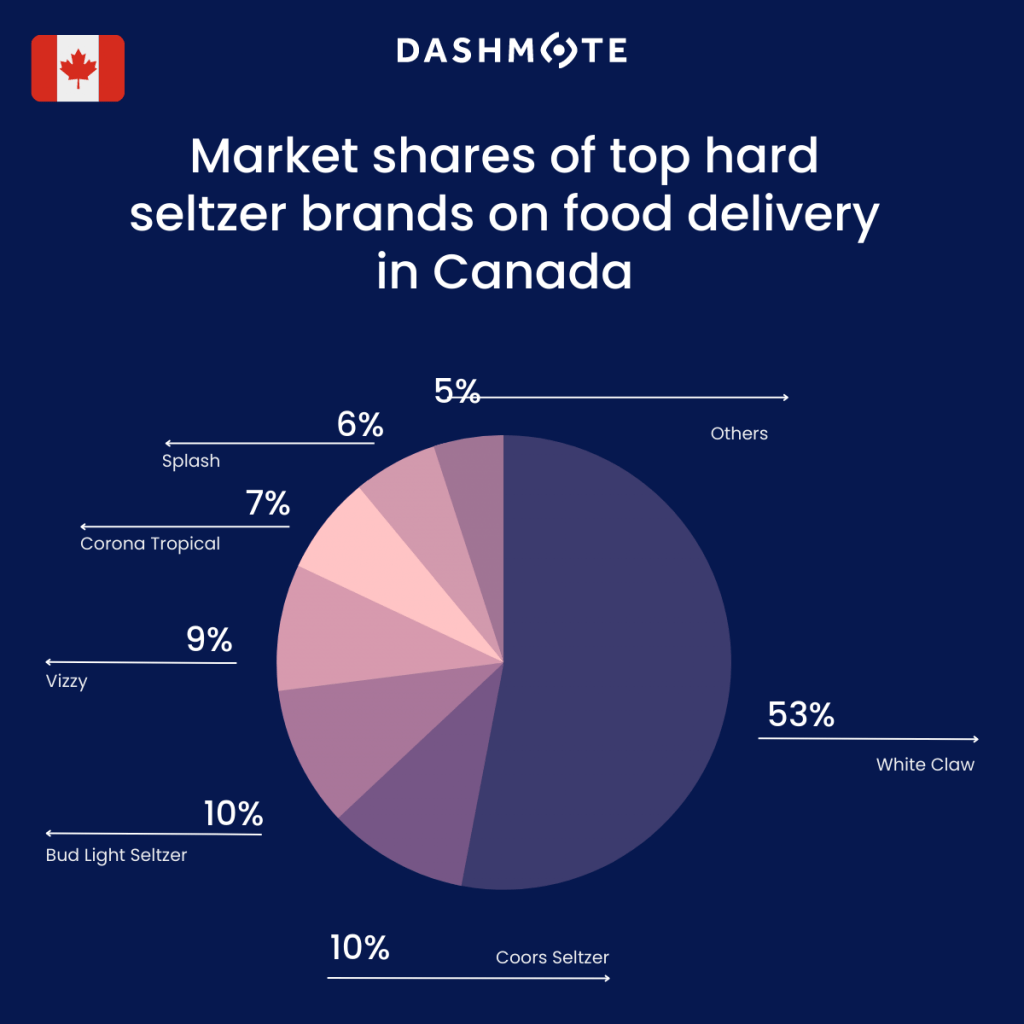

In Canada, the market for food delivery is much smaller than in the US. White Claw dominated Canadian food delivery platforms in Q4, 2022 with a 53% hard seltzer market share. There was a huge gap to the second most listed brand, Coors Seltzers, which controlled only 10% market share. The penetration rate of White Claw (1.8%) is more than 4.5 times higher than Coors Seltzer (0.4%) and Bud Light Seltzer (0.3%).

The QoQ growth of the top 5 hard seltzer brands on Canadian food delivery varied between 8% and 22% in Q4, 2022. Corona Tropical, released by AB InBev in May 2022, saw the largest growth on food delivery. This is followed by White Claw, with a 15% QoQ growth.

Speaking about the domination of White Claw in the hard seltzer market, Nicholas Greeninger, CEO of Tolago Hard Seltzer, said that he didn’t expect it to fall from the top position but he did expect smaller brands and businesses to gain more sales in the future [7]. With only less than 1% of all menu cards on Canadian food delivery having a hard seltzer product listed, we are confident that there is a major opportunity for the drinks to grow their business by expanding their presence on food delivery.

Dashmote is the leading big data and AI analytics company in the food & beverage industry. We empower F&B leaders and analysts to track and analyse publicly available data so they can make informed decisions for their brands. Do you want to know more about retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.

The quick-service restaurant (QSR) industry has been witnessing a revolutionary trend as consumers reduce dining in and utilise delivery options. Something that was initially popularised due to the pandemic seems to be sticking around. The global restaurant operators are also taking notice of it. In McDonald’s third-quarter earnings report, CEO Chris Kempczinski emphasised a digital momentum. He mentioned that digital sales now represent over one-third of systemwide sales in McDonald’s top six markets. This signifies the importance for QSRs to partner with delivery platforms to open up additional channels for consumers to access their ‘Happy Meal’ or ‘Whopper’.

As one of the top six markets of McDonald’s according to FoodService[1], Australia is also one of the biggest countries for food delivery with the most number of digital storefronts (DSFs*). In Australia, the revenue in the Online Food Delivery segment is expected to show an annual growth rate (CAGR 2022-2027) of 8.12%, resulting in a projected market volume of US$3.17bn by 2027[2]. In this article, we investigate the top QSRs in the Australian food delivery market. We aim to provide insights into the market shares and growths of these key players.

DSFs*: A DSF refers to the digital representation of a business on a food delivery platform.

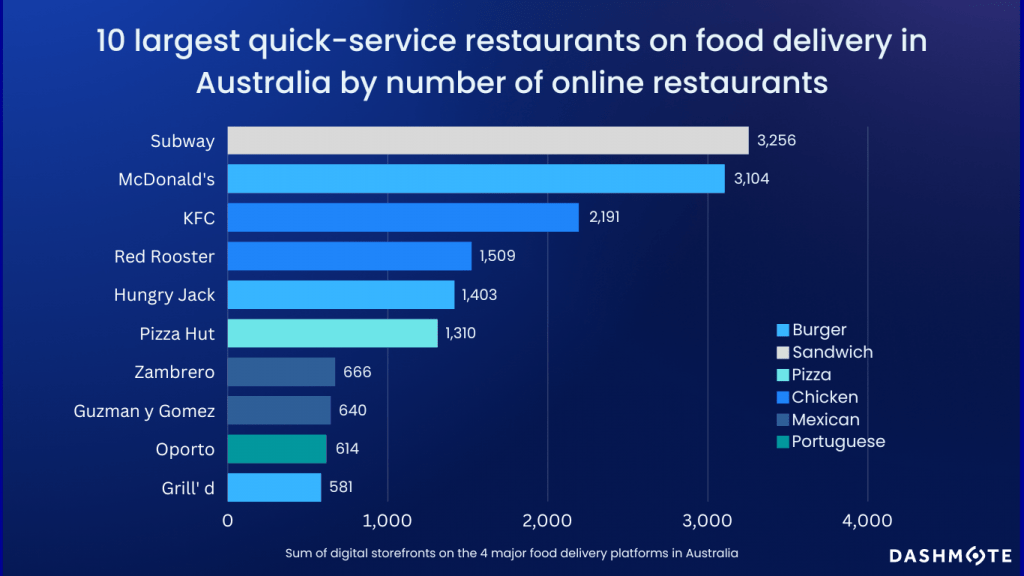

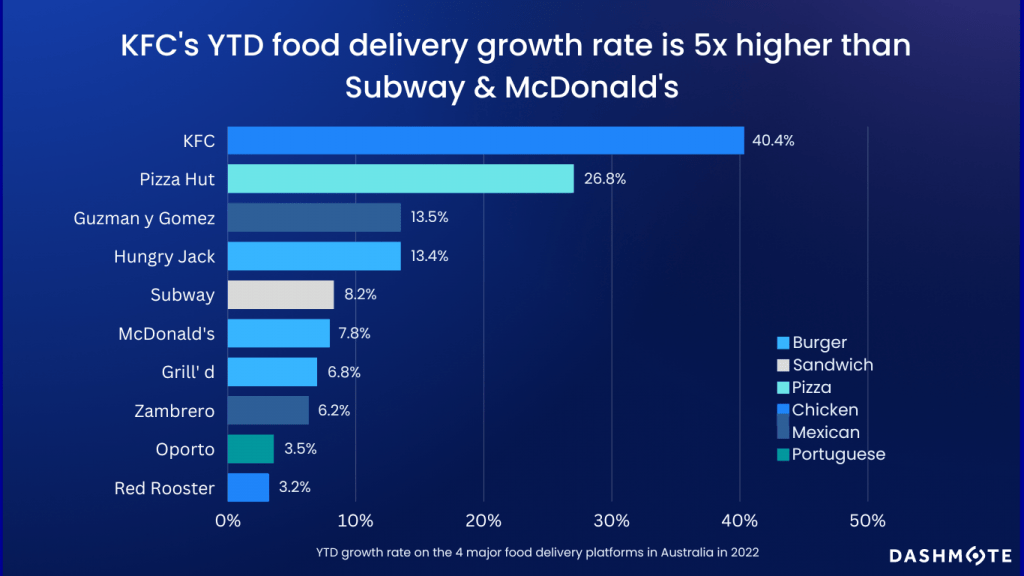

Our data reveals the top 10 QSRs on food delivery in Australia. Subway and McDonald’s are competing to be the biggest QSR — both brands have around 3K DSFs on Australian food delivery across Uber Eats, Just Eat, DoorDash, and Deliveroo. KFC, Red Rooster, and Hungry Jacks - an Australian fast food franchise of the Burger King Corporation, make up the rest of the top five brands. It’s important to note that McDonald’s, KFC, and Pizza Hut all have self-managed delivery infrastructure parallel to their presence across food delivery platforms, which to some extent might affect their strategies on these external platforms. As you can see, Domino’s is not in the top 10 since they are delivering 100% via their own infrastructure.

The top 10 QSRs on food delivery in Australia have diverse cuisine types, bringing a variety of options to Australian consumers. Burger is the most common cuisine type within the top 10 QSRs, followed by chicken and Mexican food. While the pandemic boosted the food delivery industry, the breadth of offerings becomes a key consideration that determines which brands win or lose as the industry develops. Pizza Hut’s digital co-brand WingStreet recently partnered with DoorDash in July 2022 to bring greater availability in offerings to its Australian consumers. This extension of the menu contributes to the success of the brand in Australia.

These days, it’s important for QSRs to treat off-premises guests with the same level of care and attention as those who dine inside. Achieving No.1 in YouGov’s 2022 Dining and QSR rankings in Australia[3], Subway is updating all their consumer-facing channels to enhance its feedback mechanism[4]. Among similar lines, McDonald’s has been investing in mobile-driven marketing solutions to drive digital engagement among off-premises consumers. Pizza Hut also invests largely in technology and food delivery, which has enabled the company to reduce its delivery time by 40%. By teaming up with food delivery platforms, QSRs can provide greater availability and care for their off-premises consumers.

Our data shows that there is rapid growth for most of the top 10 QSRs on food delivery in Australia in 2022. Due to a new partnership with Uber Eats in Q2 2022, the growth rate of KFC increased the most by 40.4%, which was around five times more than McDonald’s and Subway. Moreover, Pizza Hut also had a distinct increase in the number of DSFs on food delivery due to the push of WingStreet on the DoorDash platform. Overall, the remarkably stable growth of top QSR brands across three quarters in 2022 implies the dominance of fast-food franchise outlets on delivery platforms in Australia.

Today’s QSR is a multi-faceted and complicated business due to the change in consumer habits during the pandemic. Even after the lift of most COVID-19 restrictions, the popularity of ordering food online hasn’t stopped. More than just recovering from the pandemic crisis, QSR businesses, such as Subway and McDonald’s, are growing significantly again, especially in digital sales. To win the food delivery game, QSRs need to strategically partner with major platforms to increase the accessibility of the outlets in the integrated digital ecosystems. It’s essential for restaurants to keep tracking the performances of their own brands as well as their competitors to determine the next strategy.

Dashmote is the leading big data and AI analytics company in the food & beverage industry. We help F&B enterprises by empowering them to track and analyse publicly available data to making strategic decisions. Are you interested in retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.

The US is the second largest food delivery market (behind China) globally. BusinessWire indicated that the US online food delivery market reached a value of 23.4 Billion USD in 2021, and it is expected to reach 42.6 Billion USD by 2027 [1], with an annual growth rate (CAGR 2021 – 2027) of 10.5%. By analysing data from the three main delivery platforms - DoorDash, Uber Eats, and Grubhub, we are excited to provide insights into the US food delivery market.

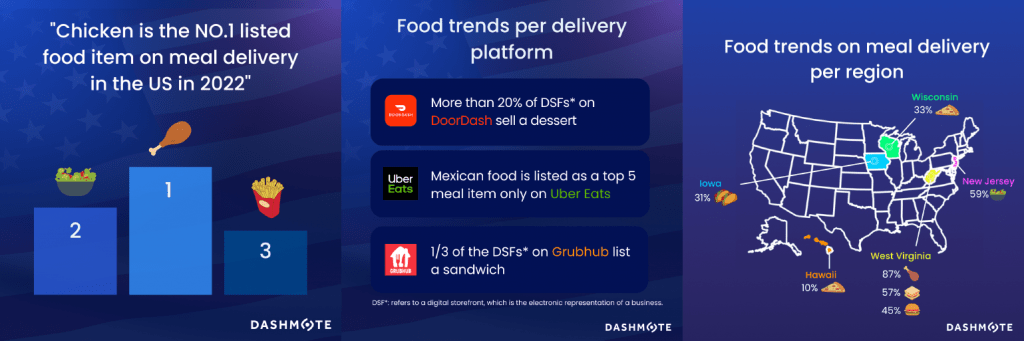

Our data reveals that chicken, salads, and fries are the top three most listed food items on food delivery in the US. Out of more than 1.3 million Digital Storefronts (DSFs*) in the US by August 2022, around 75% of all DSFs listed chicken, 50% listed salads, and 46% listed fries.

*A DSF refers to the electronic representation of a business on a food delivery platform. A business can be listed on three different food delivery platforms (e.g. DoorDash, GrubHub and Ubereats), in our data that would be counted as three DSFs and one outlet.

Our data shows that all three platforms value ease and convenience, and the top listed foods vary very slightly between these platforms. Specifically, 40% of all DSFs* on DoorDash list sandwiches, 1/3 of the DSFs on Uber Eats list rice dishes, and Grubhub has the highest % of DSFs listing desserts. Understanding the key trends and overall characteristics of food delivery platforms will benefit your business in discovering the opportunities in the market.

In the United States, West Virginia has the highest percentage of DSFs listing chicken dishes, sandwiches and burgers. New Jersey has the most DSFs listing salads. Iowa has over 1/3 of DSFs selling taco. Pizza is most popular in Wisconsin. Interestingly, Hawaii has the lowest percentage of DSFs listing pizza, which is only 10%.

Platforms such as DoorDash, Uber Eats, and Grubhub have widely opened the delivery space in the US, making it significantly easier for businesses of all sizes to sell their product online and have it delivered straight to customers. Unlocking opportunities in the complex ecosystem of the US food delivery industry requires constant tracking and analysing the latest data to gain a sophisticated understanding of where the market is heading.

If you are looking for more data insights, or interested in collaborations, please contact sales@dashmote.com.