Energy drinks are characterised by the presence of high levels of stimulant ingredients, usually caffeine, and are often marketed as products capable of enhancing mental alertness and physical performance. Appearing in the late 19th century in the form of tonic water, energy drinks today are a multi-billion dollar industry with a variety of brands and formulations available worldwide. According to industrial research, the energy drinks market was valued at 93.3 billion in 2021 and is expected to reach the value of USD 244.54 billion by 2029, at a CAGR of 12.80% during the forecast period [1].

Brands in the food and beverage industry are making every effort to capitalise on the opportunity as the trends of fitness are growing around the world. As for energy drinks companies, they greatly benefited from the increasing consumer desires for quick mental and physical energy boosts and enhancement of overall performance. To further diversify their product portfolio and to reach a larger consumer base, manufacturers are rapidly investing in new marketing strategies, including improving availability and sales in the food delivery channels.

In this article, we conducted a study on the energy drinks market in the North American food delivery industry. By leveraging Dashmote’s Data Analytics SaaS platform, we introduce key players in the industry from the perspective of food delivery penetration rates and growths. After reading this article, the readers will acquire an in-depth understanding of the performance of major energy drink brands in the competitive situation in North America.

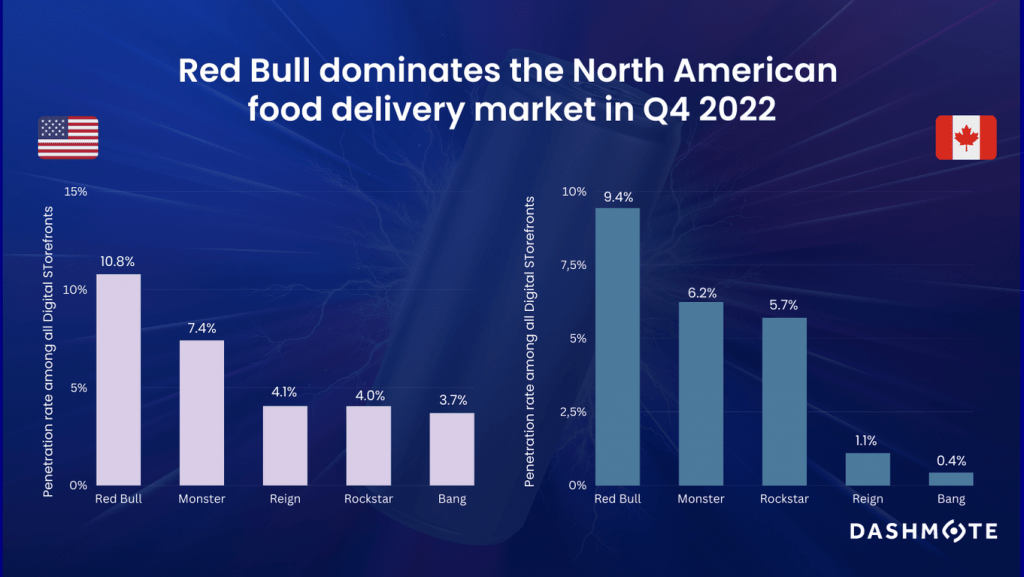

Our data shows that Red Bull dominated both US and Canadian food delivery in Q4, 2022, with a penetration rate of 10.8% in the US and 9.4% in Canada. As the first modern energy drink, Red Bull was introduced in 1987 in Austria. Today, it has a brand value of 19.96 billion Euros worldwide [2], and it has the highest brand awareness in the US [3]. As the leading energy drink brand in North America, 1 in 10 digital storefronts (DSFs) on the food delivery platform sell Red Bull. This penetration rate is higher than 7UP (6%) but lower than the majority of the soft drink brands, such as Coca-Cola (53%), Pepsi (26%) or Fanta (19%). This gap indicates the potential opportunities for Red Bull to grow its presents in the North American food delivery industry.

According to our data, the second most-listed brand on North American food delivery platforms is Monster. It had a penetration rate of 7.4% among all DSFs in the US, and 6.4% in Canada. This is followed by Reign and Rockstar in both countries. Interestingly, in the US, Reign (4.1%) and Rockstar (4.0%) had little difference in DSFs listings in Q4, 2022. However, in Canada, the total number of DSFs selling Rockstar (5.7%) is more than 5 times that of Reign (1.1%).

As shown in the above graph, overall, the existing players in the US strive to improve their market penetration rates in the food delivery industry with more equal capabilities. Whereas in the Canadian market, Red Bull, Monster, and Rockstar are dominant players.

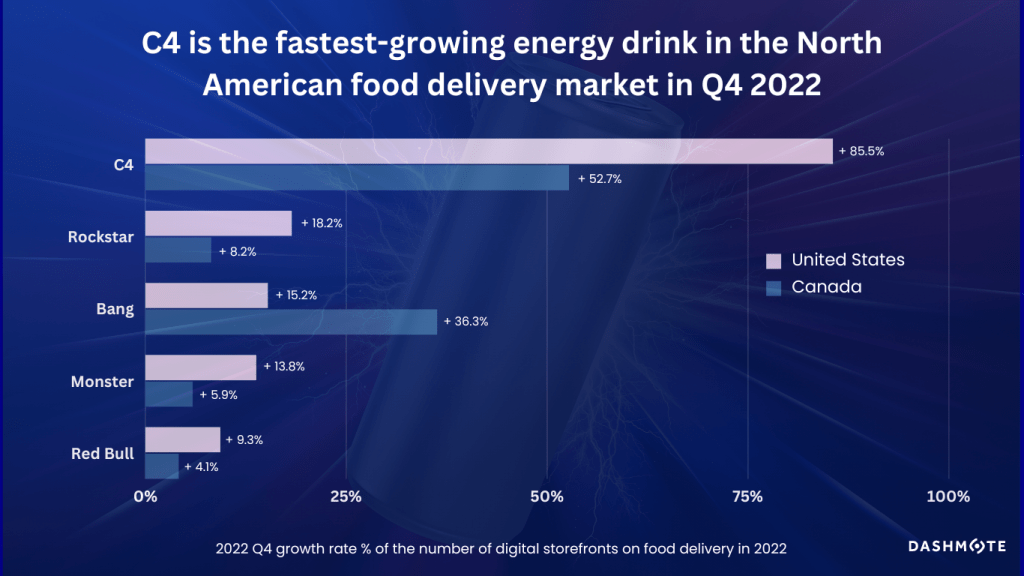

In the US, C4 energy drinks grew the most in DSFs listings by 85.5%, followed by Rockstar (18.2%), Bang (15.2%), and Monster (13.8). As the biggest market per capita volume consumption [6], the US holds a significant position in the global energy drink market. According to our data, all brands experienced positive growth in Q4, 2022 on the American food delivery platforms, indicating a flourishing market for energy drinks with growing popularity.

Among the top energy drink brands, C4 grew by 52.7% in DSFs listings in Q4, 2022, Canada, making it also the fastest-growing brand on Canadian food delivery platforms. This is followed by Bang with a 36.3% growth and Rockstar with a 8.2% growth.

According to the Energy Drinks in Canada report [4], energy drinks have experienced growth in demand in recent years due to the growing health and wellness trend. Revenue in the Energy & Sports Drinks segment in Canada amounts to US$2.01 billion in 2023 [5]. C4, along with a number of energy drink brands, are benefitting from this trend and show a significant growth in the past year. However, there are also restraints for energy brands that limit the market growth. Government restrictions and health regulations due to unhealthy image, as well as growing public awareness about the harmful effects of these drinks on children, are likely to stymie the growth of the market. In fact, according to our data, there are a number of brands experiencing a negative reduction in DSFs on Canadian food delivery platforms, such as Reign (-30,1%), NOS (-21.9%), and Full Throttle (-11.4%).

Dashmote is the leading big data and AI analytics company in the food & beverage industry. We help F&B enterprises by empowering leaders and analysts to track and analyse publicly available data to contribute to making strategic decisions for your brand. Are you curious about the non-alcoholic beverage market in the food delivery industry? Check out our data insights on non-alcoholic beer and Dr Pepper. Want to know more about retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.