Hard seltzer is a ready-to-drink beverage that blends carbonated water, alcohol, and fruit flavouring in a can for portability. The absolute explosion in interest around low and non-alcoholic beverages began during the White Claws Summer of 2019. A hard seltzer brand White Claws collaborated with comedian Trevor Wallace. Together, they released a video that popularised the phrase “ain’t no laws when you’re drinking Claws”. This line led to an explosion of growth in White Claw sales that even caused shortages across the US [1].

One year later, White Claw was still dominating the sales. At the same time, more than 150 brands were bursting out in the US in the same beverage category. This including Truly, Bud Light Seltzer, Polar Seltzer, and many more. Marketed as healthy, aspirational and gender-neutral, in 2021 the global hard seltzer market size was valued at USD 8.95 billion and is expected to expand at a compound annual growth rate (CAGR) of 22.9% from 2022 to 2030 [2].

The boom of this new drink category has greatly benefited from the outbreak of the COVID-19 pandemic. Back then, consumers started to gain higher health consciousness and look for low-alcohol beverages. Moreover, millennials and the younger generation during lockdown were driven to look for novelty on the shelves at grocery stores, and the colourful, fruity-flavoured, low alcohol and calorie seltzers were the perfect eye-catcher [3]. However, in July 2022, while crowds were returning to bars and restaurants, hard seltzer sales in retail stores were down about 18%, compared to the previous year [4]. Today, some argue that this type of drinks has lost its fizz. Others expect the market to be continuously expanding into a competitive landscape.

This article provides insight into the above controversy by leveraging Dashmote’s Data Analytics SaaS platform. In this article, we evaluated the performance of the major brands on food delivery in North America. We analyzed the data from 3 perspectives: the growths, the penetration rates and the market shares in 2022.

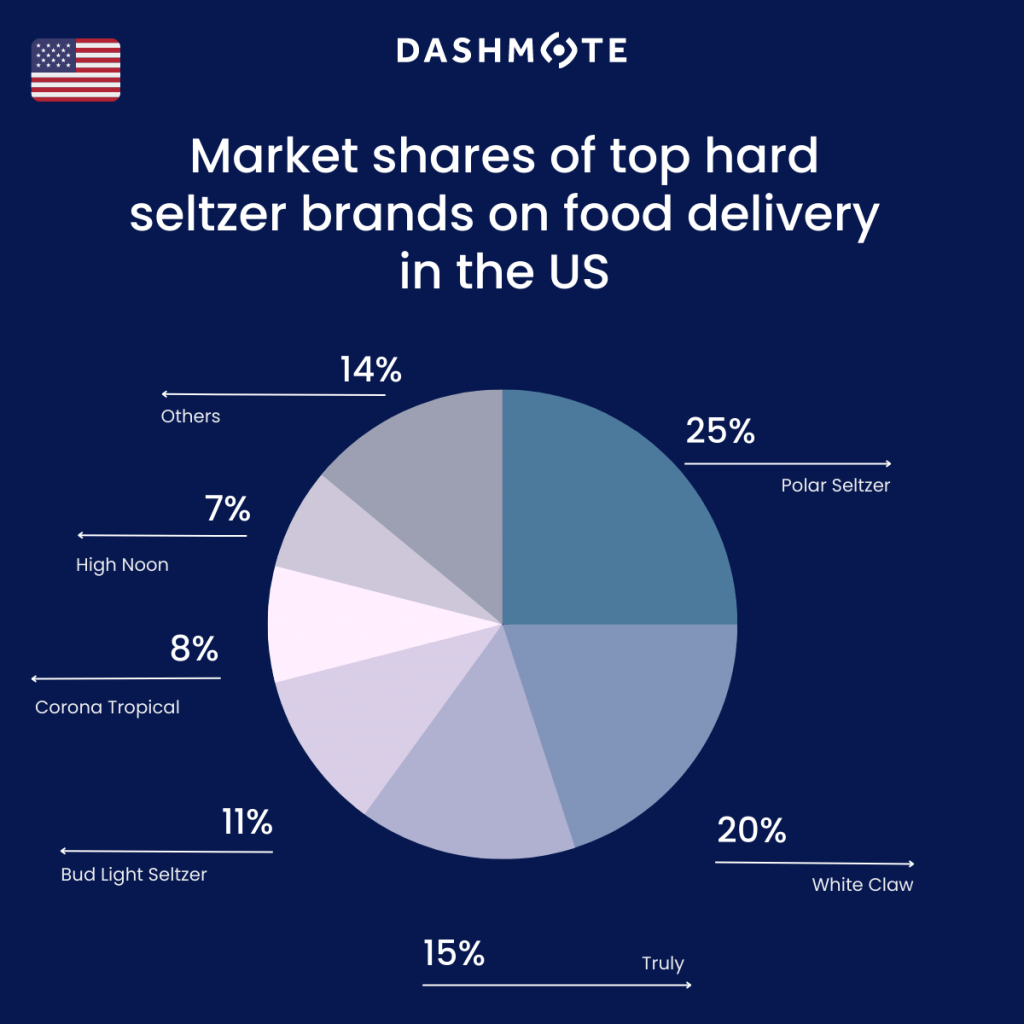

North America accounted for the largest hard seltzer revenue share of more than 55.5% in 2021 and is likely to further increase the consumption of hard seltzer in the coming years [5]. According to Dashmote’s latest data, the most listed brand on US food delivery platforms in Q4, 2022 was Polar Seltzer. It has a market share of 25% among all the Digital Storefronts (DSFs) selling hard seltzers. This was followed by White Claw, with a market share of 20%, and Truly (15%). The top 3 brands all had a penetration rate above 1% among all the DSFs in the US. Specifically, they were 2.1% (Polar Seltzer), 1.7% (White Claw), and 1.3% (Truly).

Topo Chico, bought by Coca-Cola in 2017, saw the largest quarter-over-quarter (QoQ) growth of 49% in DSFs listings in Q4, 2022. Controlling a 6% hard seltzer market share on US food delivery, Topo Chico ranked 7th among the top hard seltzer brands.

Wine and Spirit Industry Giant E&J Gallo Winery launched High Noon in 2019. It also saw a large QoQ growth of 41% and controlled 7% hard seltzer market shares in Q4, 2022. High Noon separates itself by appealing to the better-for-you crowd, including distilled liquor and real juice in its transparent ingredient list [6]. This marketing strategy appears to be successful, as proved by the growth rate in our data.

Furthermore, White Claw, Truly, and Bud Light Seltzer, all had a QoQ growth above 20%. A key takeaway from this is that the hard seltzer industry is unlikely to fizzle out in the upcoming years. Although appearing as a summertime drink, the hard seltzer market tends to remain dynamic all year round in 2022. In fact, the penetration rates of top hard seltzer brands on US food delivery are already more than 10 times higher than non-alcoholic beers, but still mainly under 2%. Partnering with restaurants and major delivery aggregators would be beneficial for hard seltzer brands to expand their digital footprints.

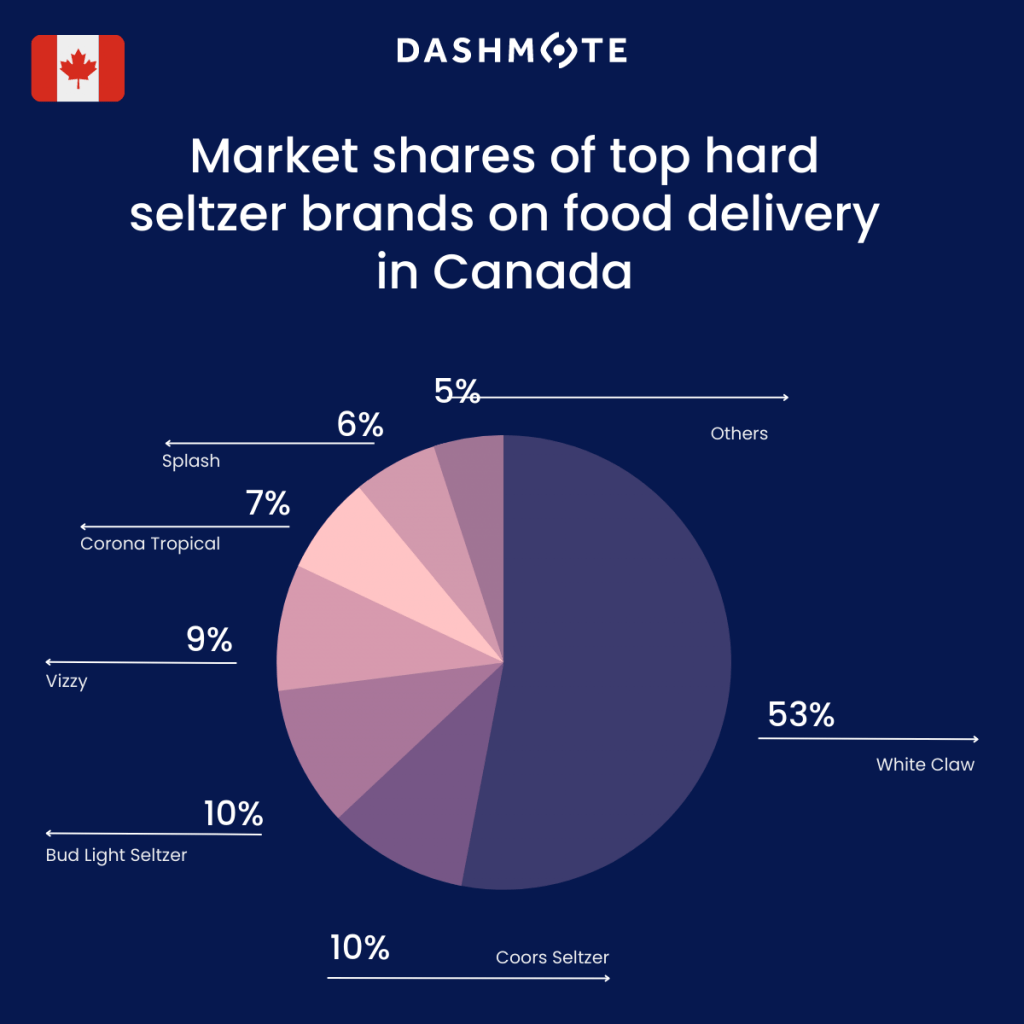

In Canada, the market for food delivery is much smaller than in the US. White Claw dominated Canadian food delivery platforms in Q4, 2022 with a 53% hard seltzer market share. There was a huge gap to the second most listed brand, Coors Seltzers, which controlled only 10% market share. The penetration rate of White Claw (1.8%) is more than 4.5 times higher than Coors Seltzer (0.4%) and Bud Light Seltzer (0.3%).

The QoQ growth of the top 5 hard seltzer brands on Canadian food delivery varied between 8% and 22% in Q4, 2022. Corona Tropical, released by AB InBev in May 2022, saw the largest growth on food delivery. This is followed by White Claw, with a 15% QoQ growth.

Speaking about the domination of White Claw in the hard seltzer market, Nicholas Greeninger, CEO of Tolago Hard Seltzer, said that he didn’t expect it to fall from the top position but he did expect smaller brands and businesses to gain more sales in the future [7]. With only less than 1% of all menu cards on Canadian food delivery having a hard seltzer product listed, we are confident that there is a major opportunity for the drinks to grow their business by expanding their presence on food delivery.

Dashmote is the leading big data and AI analytics company in the food & beverage industry. We empower F&B leaders and analysts to track and analyse publicly available data so they can make informed decisions for their brands. Do you want to know more about retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.