Pringles is a brand of potato chips (also known as crisps in British English) that has been a popular snack since its introduction in 1968. Over the years, the brand has undergone many changes and innovations to adapt to evolving consumer preferences and maintain its position in the competitive snack market. In 2012, the brand was sold to Kellogg Company, which has been the owner and manufacturer of Pringles ever since. Kellogg's is a multinational food company that produces a variety of popular breakfast cereals, snacks, and convenience foods. With the acquisition of Pringles, Kellogg's expanded its product line and strengthened its position in the global snack food market. Today, Pringles is a popular snack enjoyed by people of all ages in many countries around the world.

Pringles, the well-known potato chip brand, was created by Alexander Liepa, a Procter & Gamble chemist and food scientist who originally marketed it as "Newfangled Potato Chips". Liepa's goal was to invent a new type of potato chip that would have a uniform size and shape and wouldn't crumble or break during transport. To achieve this, Liepa developed a process where potato flakes were cooked and then pressed into the tube-shaped containers we recognize today. The result was a chip that was uniform in shape and could be stacked neatly in the container without breaking or crumbling. When Pringles was launched nationally, the name was changed to what we know it as today. Procter & Gamble opted for the name "Pringles'' after finding it in a Cincinnati phone book. The company was attracted to the pleasant sound of Pringle Avenue in Finneytown, Ohio.

When Pringles was first introduced, it was marketed as a new kind of chip that was different from traditional potato chips. The brand was successful, and quickly became popular in the United States and around the world.

Over the years, the brand has introduced many different flavors and varieties of chips, including sour cream and onion, cheddar cheese, and BBQ. The brand has also experimented with different packaging sizes, from small snack-sized containers to large party-sized containers.

In recent years, Pringles has continued to innovate in order to stay relevant in the age of food delivery. The brand has introduced new flavors and packaging sizes that are designed to appeal to people who are looking for convenient and portable snacks.

One of the ways that Pringles has adapted to the changing food delivery landscape is by partnering with food delivery companies. Pringles has teamed up with companies like Uber Eats and DoorDash to offer special promotions and deals on their products.

Pringles has also embraced e-commerce, and now offers their products for sale on their website as well as on other online retailers like Amazon. This makes it easy for people to order Pringles from the comfort of their own homes and have them delivered directly to their doorstep.

In the UK, a captivating trend has emerged as the presence of Pringles in digital storefronts has grown remarkably. In Q3 2021, Pringles accounted for around 3% of all digital storefronts. By Q1 2023, this figure had risen to over 6%, with more than 9000 new stores joining the Pringles wave. A similar story unfolded in the US, where Pringles' market share increased from around 4% in Q3 2021 to over 5% in Q1 2023.

Meanwhile, in Canada, Pringles' market share rose from just over 2% in Q4 2021 to above 3% in Q1 2023. Australia experienced a more fluctuating trend, peaking at almost 4.5% in Q4 2021 before settling at just under 4% in Q1 2023. This data paints a picture of Pringles' digital storefronts rapidly expanding, particularly in the UK, where the market share more than doubled in less than two years.

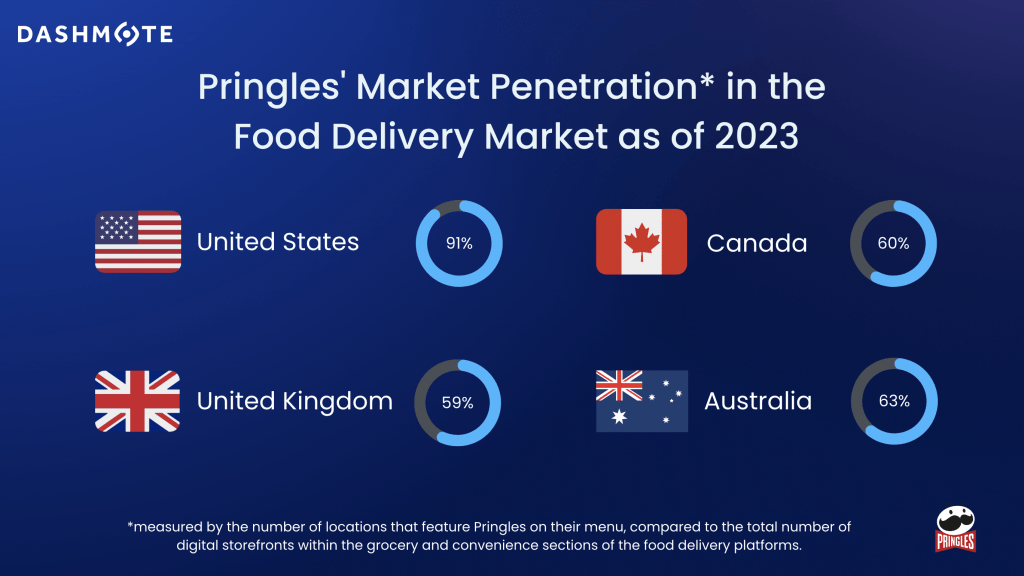

Taking a closer look at Pringles' presence on UberEats platforms within the convenience and grocery stores, the data reveals promising growth. For instance, in the US, 90% of the digital stores are selling Pringles. In Australia, Pringles' market share increased from 49% in Q1 2022 to 63% in Q1 2023. Similarly, in Canada, the market share witnessed an upsurge from 41% in Q4 2021 to 60% in Q1 2023. It's clear that more and more stores and with that also people are choosing Pringles as their go-to snack when ordering online.

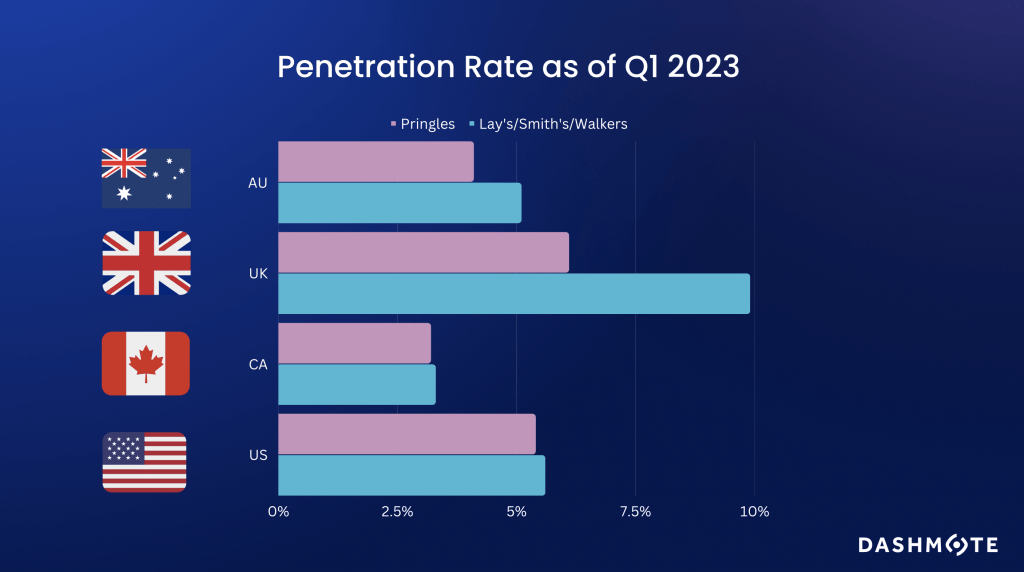

While Lay's, Smith's, and Walkers are essentially the same potato chip brand owned by PepsiCo, each caters to different markets under different names: Lay's in the US, Walkers in the UK and Smith's in Australia. Although each version of the brand has unique flavors and ingredients tailored to local preferences, they all share the same parent company, PepsiCo, which acquired Frito-Lay in 1965. In various regions around the world, these chips are also sold under other names, such as Chipsy in Egypt and the West Balkans, Tapuchips in Israel, Margarita in Colombia, and Sabritas in Mexico [1, 2] .

Pringles, owned by Kellogg's, faces diverse competitive landscapes in different regions when compared to its PepsiCo-owned counterpart, which is known as Lay's, Smith's, or Walkers depending on the market. Market penetration varies across regions, reflecting the unique challenges and opportunities Pringles encounters as it seeks to expand its global presence in the snack industry.

In the US, Pringles holds a 91% market penetration in convenience and grocery stores, with which it is outcompeting Lay's which has a penetration rate of 88%. In Australia, Pringles is available at 63% of the grocery and convenience digital storefronts, while Smith's is available at 78%, indicating room for growth for Pringles. In the UK, Pringles stands at 59% market penetration, while Walkers, its main competitor, holds a stronger 76%, signaling potential for expansion. In contrast, the Canadian market sees Pringles with a 60% market penetration, almost on par with Lay's at 62%.

Dashmote excels in big data and AI analytics for the F&B sector, empowering professionals to leverage public data for strategic decisions. Curious about the snack market on food delivery? Explore our insightful data on chocolate. Want to know more about retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.

Chips, also referred to as crisps in the UK, are thin snacks that are seasoned and fried till crisp. Invented in 1853 in New York, chips today are one of the most extensively consumed snacks across the world. This high demand are still rising continuously and significantly. Statistics show that the global Chips Market is likely to grow with a CAGR of 3.92% from 2020-2028, and is projected to reach US$ 43.8 Billion by 2028 [1].

As chips became a regular part of many consumers’ diets, manufacturers and marketers are seeking to expand their channels digitally to reach a wider consumer base. Although the Supermarket category currently still holds the most significant shares in sales and distributions of chips, the Online Retailing category is expected to be the fastest expanding segment over time [2]. This growth is due to the greater availability of a wide selection of flavours, faster accessibility, and the easy cost comparison of different chip products across the platform.

Food delivery platforms nowadays are an increasingly common way for consumers to purchase groceries, including chips. In this article, we generate food delivery insights in 2022 which reflect the digital trends and opportunities shaping the chips industry. By leveraging Dashmote’s Data Analytics SaaS platform, we analysed the penetration rates and growths of top chip brands and manufacturers on food delivery platforms in the US and UK.

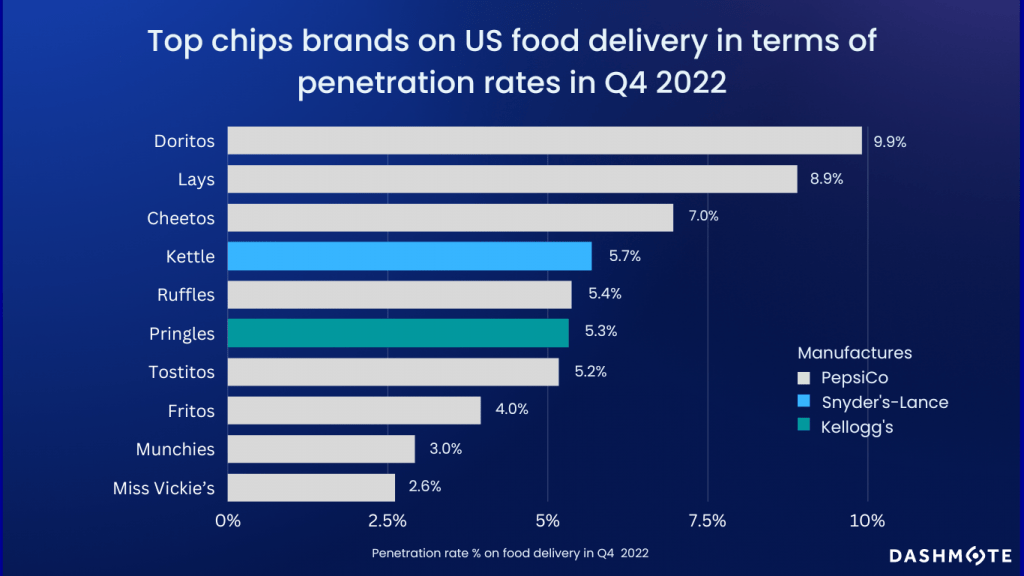

Our data show that the most listed chip brand on US food delivery in 2022 was Doritos. It has a 9.9% penetration rate among all the Digital Storefronts (DSFs) on food delivery. Lay’s (8.9%) and Cheetos (7.0%) are following in the ranking. PepsiCo, Synder’s-Lance, and Kellogg’s are the key players in the market. Remarkably, PepsiCo manufactures 8 out of 10 top chip brands on US food delivery. This indicates its dominant position in the digital space of chips.

PepsiCo was established in the US in 1965. Today, it is present in nearly 200 countries. It focuses on launching new products in order to gain maximum market share [3]. In January 2021, PepsiCo launched its Doritos Flamin Hot Cool Ranch flavoured potato chips. These innovative flavours certainly contributed to brand visibility across the globe. Kellogg’s is another major player in the potato chip industry. It focuses on business model transformation to enhance performance and increase long-term shareowner value. In fact, in 2022 Kellogg’s planned to separate into three independent companies [4]. This transformation helped the company to enhance its production capacity and resources toward its leading snack brands, such as Pringles.

The existing players strive on improving their market shares in the food delivery industry. In the top 10 chip brands, Tostitos grew the most in digital storefront listings by 22% in Q4 2022. This is followed by Fritos with a 20% growth and Ruffles with a 17% growth. All 3 brands are owned by PepsiCo, representing the strong profitability of its iconic brands on food delivery. Moreover, 9 out of the top 10 brands saw a positive growth between 7% to 22% in Q4, 2022. This indicates a flourishing digital market space for chips on US food delivery.

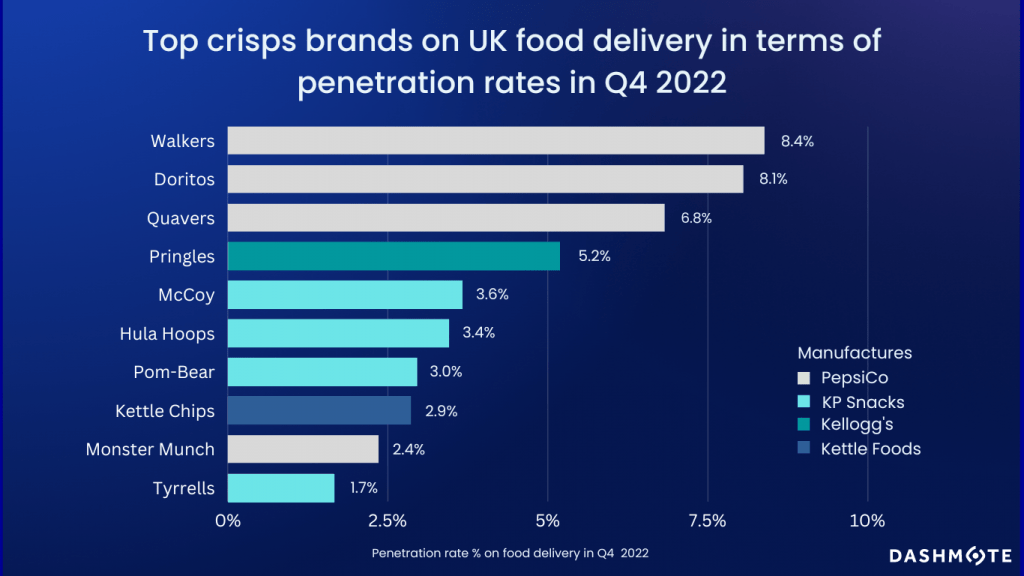

In the UK, Walkers, Doritos, and Quavers are the top 3 crisp brands on food delivery in terms of DSFs listings. They are all manufactured by PepsiCo, with a penetration rate between 6.8% to 8.4% among all DSFs in Q4, 2022. Unlike the domination of PepsiCo in the top 10 chip brands on US food delivery, in the UK, the British company KP Snacks is quickly catching up with 4 of its leading brands. It is clear from our data that, after investing $7.5 million into opening a new production site for its Pom-Bear and Hula Hoops Puft brands in 2019 [5], these brands are showing strong growth momentum and profitability in the digital space.

Let’s now talk about growth. According to Dashmote’s data, Pom-Bear grew the most by a staggering 133% on food delivery in terms of DSFs listings in Q4 2022. Tyrrells (55%), a premium brand also from KP Snacks, and Monster Munch (35%) from PepsiCo are following. All top 10 brands saw positive growth in Q4 2022, which indicates that there are significant opportunities in the food delivery industry for crisp brands’ long-term category prospects and further expansions.

For chips brands, food delivery serves as an additional channel to reach a wider consumer base. Food delivery can add chips as a convenient food option for a number of reasons. Firstly, chips are easy to transport with their own packages. Secondly, it always stays crispy, compared to french fries that lose crispness during transportation. Thirdly, restaurants can ass chips as a combo deal to provide variety to the meals and add great margin to the restaurants. Therefore, we anticipate supplies of chips to rise further on food delivery across the globe.

Dashmote is the leading big data and AI analytics company in the food & beverage industry. We help F&B enterprises by empowering leaders and analysts to track and analyse publicly available data to contribute to making strategic decisions for your brand. Do you feel interested in the snack market on food delivery? Check out our data insights on chocolates. Want to know more about retrieving market insights across food delivery and F&B?

→ Please contact sales@dashmote.com.